A defining economic fault line is opening ahead of the 2026 election — and it is not merely about jobs, but about what kind of country Sweden intends to become

As Sweden approaches the 13 September 2026 Riksdag (parliamentary) election, the labour market has emerged as the defining political battleground — and the numbers tell a story that transcends conventional partisan blame. With unemployment hovering at 8.6% seasonally adjusted in April 2026, according to Statistics Sweden (SCB), the country sits at the 27th position among 29 European nations, wedged between Finland at 28th and Spain at the bottom. The Nordic “model” that once commanded global admiration has fractured into two distinct realities: a resource-rich north facing labour shortages, and a deindustrialising south grappling with structural unemployment that rivals Southern Europe. For senior executives, institutional investors, and policymakers watching the region, the question is no longer whether Sweden can fix its labour market — it is whether the political system can agree on what “fixing” actually means.

The Headline and the Reality

At first glance, Sweden’s unemployment figures appear unambiguously troubling. The smoothed, seasonally adjusted rate of 8.6% in April 2026 places the country firmly in Europe’s bottom tier, a position that would have been unthinkable a decade ago. Yet headline figures conceal as much as they reveal. Sweden’s Labour Force Surveys (LFS), conducted under strict International Labour Organization (ILO) standards, count full-time students actively seeking part-time work as unemployed — a methodological choice that inflates the headline rate significantly. Of the roughly half a million individuals registered as unemployed, more than 140,000 are full-time students. Adjust for this technicality, and the “core” unemployment rate looks markedly different.

This is not an argument for complacency. Rather, it underscores a deeper truth: Sweden’s labour market challenge is structural, not merely cyclical. The country maintains one of the highest employment and labour-force participation rates in the European Union — approximately 75% of the population aged 15–74 is either working or actively seeking work. The problem is not a lack of willingness; it is a structural matchmaking failure between what the economy demands and what the labour force supplies.

The Insider-Outsider Divide

Swedish employment data reveal a labour market cleaved in two. For native-born Swedes aged 20–66, unemployment sits at a relatively manageable 5.0%. For foreign-born residents, the figure is 14.5% — nearly three times higher. This disparity is not unique to Sweden, but its magnitude is striking even by European standards and carries profound implications for social cohesion, fiscal sustainability, and long-term growth.

The roots of this divide are multifaceted. Sweden’s economy is among the most digitised and knowledge-intensive in the world, with strong collective bargaining agreements that establish a high wage floor. The result is a “skills barrier” that few other European economies replicate: there are virtually no low-skilled, entry-level “mini-jobs” of the kind that exist in Germany or the Netherlands. Fluent Swedish and specific technical credentials are prerequisites for meaningful labour-market entry. For immigrants lacking these assets — particularly those arriving with limited formal education or non-European qualifications — the barriers to entry are formidable.

This is not simply a humanitarian concern. The fiscal implications are substantial. High unemployment among foreign-born populations strains municipal budgets, particularly in regions with concentrated settlement patterns. It also represents a significant drag on potential GDP growth at a time when Sweden’s working-age population is ageing and the old-age dependency ratio is climbing steadily across the Nordic region.

Five Years of Drift: From Post-Pandemic Rebound to Structural Stagnation

The trajectory of Swedish unemployment over the past half-decade illustrates the interplay between cyclical and structural forces. The post-pandemic recovery of 2022, which saw unemployment fall to 7.4%, proved short-lived. By 2024, a technical recession, the collapse of the construction sector, and a broader European manufacturing slowdown had pushed the rate back to 8.5%. The peak of 8.9% in 2025 marked the nadir of the cyclical downturn, with the gap between Sweden and the European average widening to levels not seen in a generation.

A five year look at Y/Y swedish unemployment. Data visual is open in a new tab

The stabilisation seen in early 2026 offers modest relief, but long-term unemployment — those out of work for more than 12 months — remains particularly stubborn. This is the segment of the labour market least responsive to cyclical recovery and most dependent on structural reform. For investors and corporate strategists, the signal is clear: Sweden’s labour market is unlikely to self-correct through macroeconomic tailwinds alone.

The Nordic Divergence: A Model No Longer Uniform

The notion of a unified “Nordic model” has become an anachronism. Data from the State of the Nordic Region and Nordic Insights highlight a dispersion that would have been inconceivable a decade ago. Iceland and Norway maintain structurally low unemployment — 4.0% and 4.5% respectively — placing them among Europe’s strongest performers. Denmark, at 6.4%, sits above the EU average but retains a dynamic labour market. Sweden and Finland, meanwhile, have drifted toward bottom-tier European performance, with Finland now ranking second-worst in the EU behind only Spain.

Regional distribution of employment and unemployment in Sweden. Data visual is open in a new tab.

What explains this divergence? Three distinct models are at work.

Denmark’s “Flexicurity” makes it exceptionally easy for employers to dismiss workers, which paradoxically encourages hiring by reducing the risk of a bad match. In exchange, the state provides robust safety nets and mandatory, aggressive retraining programmes from day one of unemployment. Sweden’s employment protection legislation (Lagen om anställningsskydd, or LAS), by contrast, makes employers hesitant to take chances on unproven candidates — particularly in a high-wage environment where mistakes are costly.

Norway’s resource and public-sector buffer provide a degree of economic insulation that Sweden cannot replicate. The Government Pension Fund Global, built on decades of petroleum revenues, underwrites countercyclical spending, while a large public sector absorbs labour during downturns. Norway’s integration challenges are also smaller in scale relative to total population.

The collective agreement barrier is perhaps the most politically sensitive distinction. Sweden’s union-driven wage model makes the implementation of statutory “subminimum wages” for training or entry-level positions structurally and politically impossible. While this protects wage integrity and reduces in-work poverty, it also limits the flexibility that Denmark deploys to shift workers between declining and growing sectors. For a knowledge-intensive economy with limited low-skilled job openings, this trade-off carries significant consequences.

The Political Calculus: Supply-Side Incentives vs. Demand-Side Integration

The 2026 election will ultimately be a referendum on which diagnosis of Sweden’s labour market failure is correct — and therefore which remedy to apply. The ideological split is sharp and well-defined.

The Tidö Bloc — comprising the Moderate Party, Christian Democrats, Liberals, and Sweden Democrats — advances a supply-side argument. Its proposed “benefit ceiling” (bidragstak) and tax reductions for low-income earners are designed to widen the financial gap between living on benefits and working, thereby incentivising labour-market entry. Stricter language and cultural integration requirements form the complementary pillar. The compelling aspect of this approach is its fiscal realism: it directly addresses the sustainability of the welfare state and creates immediate incentives for employment. The weakness is equally apparent — lowering benefits does not create jobs in an economy structurally short of low-skilled positions. The risk is not merely theoretical: without parallel job creation, vulnerable groups may be driven into poverty rather than employment.

The Opposition Bloc — led by the Social Democrats with support from the Green Party, Left Party, and Centre Party — argues that unemployment is a structural mismatch, not a motivational deficit. Its prescription is massive public investment in green industrial transitions, heavily subsidised regional upskilling, and state-funded “transition jobs” (etableringsjobb). The logic is sound for a high-tech economy that inherently demands a highly educated workforce: the state must build the educational bridges to move workers from declining sectors into healthcare, education, and green energy. The weakness is equally structural — it is extraordinarily expensive, requires years to yield results, and depends on public-sector expansion that can be slow to adapt to rapidly shifting market demands.

The choice between these frameworks is not merely ideological; it reflects fundamentally different assessments of where the bottleneck lies. If the primary constraint is individual incentive and labour cost, the Tidö approach is the more coherent fit. If the constraint is structural education and industrial mismatch, the Social Democratic framework offers the more systematic response. For international observers, the critical insight is that neither approach can succeed in isolation — and the political arithmetic of Sweden’s fragmented party system makes a synthesis unlikely before 2026.

The Geographic Fracture: Two Swedes, Two Economies

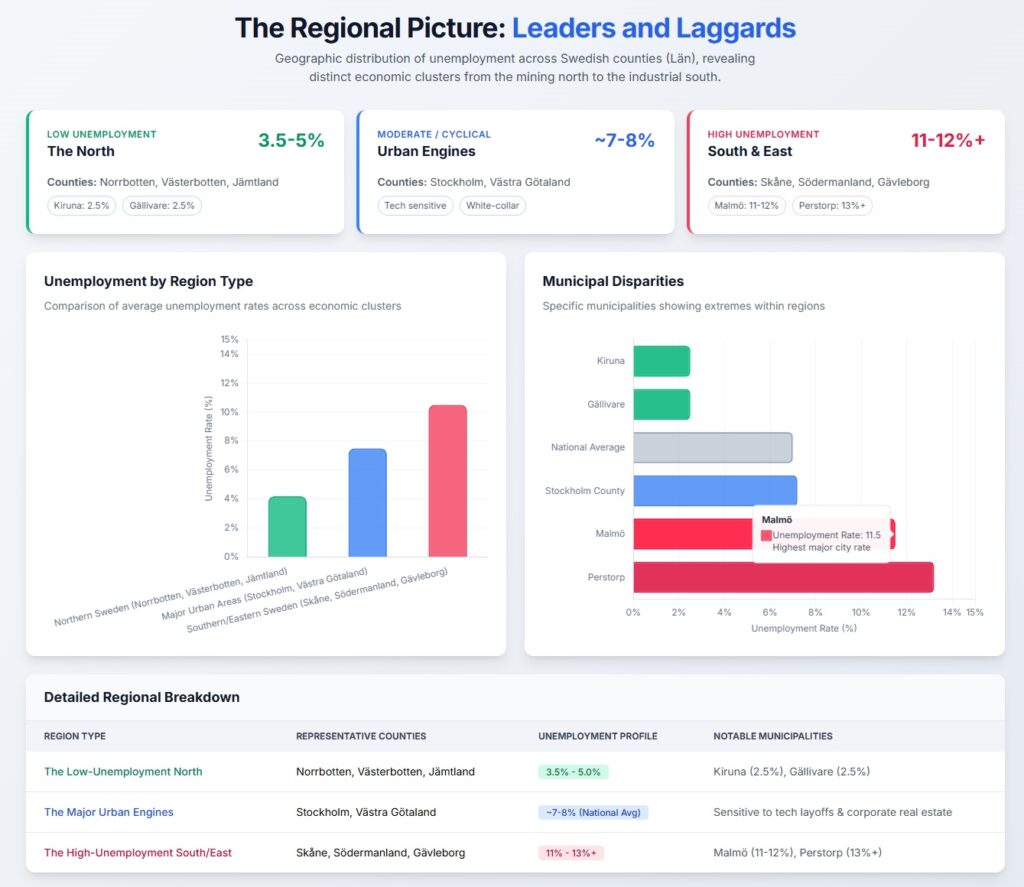

Perhaps the most underappreciated dimension of Sweden’s labour market crisis is its profound regional asymmetry. Viewing Sweden as a single macroeconomic entity obscures a geographic divergence that is reshaping the country’s political and economic geography.

The Low-Unemployment North — Norrbotten, Västerbotten, and Jämtland — reports unemployment rates between 3.5% and 5.0%, with specific municipalities such as Kiruna and Gällivare hovering around 2.5%. These regions are not merely outperforming the national average; they are experiencing acute labour shortages. The driver is the green industrial revolution: multi-billion-kronor investments in fossil-free steel (H2 Green Steel, now Stegra, and the HYBRIT consortium of SSAB, LKAB, and Vattenfall), battery manufacturing (Northvolt’s ecosystem), and green mining have transformed local labour markets. The primary challenge is no longer finding jobs for workers, but finding workers for jobs.

The High-Unemployment South and East — Skåne, Södermanland, and Gävleborg — presents the mirror image. Skåne regularly records the highest regional unemployment rates, with Malmö pushing past 11–12% and industrial hubs like Perstorp seeing figures above 13%. These regions are vulnerable to cyclical downturns in traditional manufacturing and logistics, and the construction collapse of 2023–2024 hit them disproportionately hard.

The Major Urban Engines — Stockholm and Västra Götaland — sit in the middle, with unemployment slightly below or matching the national average. These regions are highly sensitive to white-collar tech layoffs and corporate real estate corrections, but retain deeper labour-market liquidity than their southern counterparts.

The drivers of this gap are fourfold.

First, the green industrial revolution in the north has created demand that local supply cannot meet.

Second, structural deindustrialisation and the real estate slump have penalised southern economies dependent on construction and traditional engineering. Third, demographic disparities mean that regions such as Skåne have absorbed disproportionate shares of foreign-born populations, creating an “integration queue” that local service-sector economies cannot absorb quickly.

Fourth, and most critically, labour mobility is severely constrained: the north faces acute housing shortages, and the specialised skills required for hydrogen steel production or automated mining do not map neatly onto the profiles of displaced retail, construction, or assembly workers from the south.

For the 2026 campaign, this regional disparity fundamentally alters electoral strategy. The opposition will point to southern unemployment as evidence of failed national economic management. Northern regional leaders, meanwhile, are demanding state funding for infrastructure, housing, and transport links to help them absorb the rest of the country’s available labour — a demand that carries significant fiscal implications.

The Strategic Stakes

Sweden’s labour market crisis is not a transient cyclical episode. It is the manifestation of deeper structural tensions: between a high-skill, high-wage economy and a population with unevenly distributed human capital; between a generous welfare state and the fiscal pressures of an ageing society; between regional economic divergence and a political system designed for national consensus. For internationally minded business leaders, the implications are substantial.

Investment climate: The divergence between north and south creates a two-speed investment environment. Green industrial projects in Norrbotten and Västerbotten offer compelling long-term opportunities, but are constrained by infrastructure bottlenecks and labour shortages. Southern Sweden, meanwhile, presents value opportunities in distressed assets but carries higher structural risk.

Workforce strategy: Companies operating in Sweden must plan for persistent skills shortages in technical and engineering roles, coupled with surpluses in administrative and lower-skilled service positions. The absence of a German-style dual vocational training system exacerbates these mismatches.

Regulatory and policy risk: The 2026 election outcome will determine whether Sweden moves toward Danish-style labour-market flexibility or doubles down on state-led industrial and educational investment. Neither path is without risk, and the fragmented party system makes radical reform unlikely — but incremental shifts will matter for labour costs, hiring practices, and sectoral subsidies.

Geopolitical dimension: Sweden’s NATO accession and the broader rearmament of European defence create additional labour-market pressures. The defence industrial base — concentrated in southern and central Sweden — will compete with green industry for skilled engineering talent, while the public sector will face competing demands for fiscal resources.

Conclusion: The Election as Inflection Point

Sweden’s labour market has reached an inflection point that transcends the 2026 election cycle. The country possesses the institutional capacity, educational infrastructure, and innovative capacity to address its structural challenges. What remains uncertain is whether its political system can forge a consensus on the necessary trade-offs — between wage protection and labour-market flexibility, between regional equity and economic efficiency, between short-term fiscal consolidation and long-term human capital investment.

The Nordic divergence is a warning: models that appear robust in aggregate can conceal dangerous fractures beneath the surface. Sweden’s challenge is not merely to reduce unemployment, but to rebuild a labour market that can integrate its diverse population, adapt to technological disruption, and sustain the welfare-state compact that has defined its national identity. The 2026 election will not resolve these tensions, but it will determine which path the country commits to pursuing. For investors, executives, and policymakers with stakes in the Nordic region, the watchword is vigilance: the Sweden of 2027 may look markedly different from the Sweden of today.

Editorial Outlook

Follow-Up Angle: “The Green Labour Crunch: Can Sweden’s North Build the Workforce of the Future?”

Sweden’s northern regions are experiencing an unprecedented industrial boom driven by green steel, battery manufacturing, and critical mineral extraction. Yet this transformation is colliding with acute labour shortages, housing deficits, and infrastructure constraints that threaten to cap the region’s growth potential. A follow-up article should examine the specific workforce strategies being deployed — from international recruitment and vocational retraining to public-private partnerships in housing and transport — and assess whether Sweden’s green industrial ambitions are structurally achievable without a fundamental rethink of labour mobility, immigration policy, and regional development funding. The piece would offer senior executives and institutional investors a granular analysis of where the Nordic green transition is delivering returns, where it is hitting hard constraints, and what the bottlenecks mean for capital allocation in the decade ahead.

This article was prepared for Nordic Business Journal. For further insights, strategic analysis, partnership inquiries, or editorial discussion, readers are invited to connect with our editorial team. Nordic Business Journal welcomes contributions from senior executives, policymakers, and institutional investors engaged with the Nordic and Baltic business landscape.

© Ganye Kwah D. for Nordic Business Journal. All rights reserved.