For decades, Sweden has been synonymous with high living standards, robust social welfare, and competitive compensation. It was a given that the Swedish labour market sat near the pinnacle of the European hierarchy. However, recent data suggests a structural shift that business leaders and policymakers can no longer ignore. Sweden is not merely stagnating; it is actively losing ground in the European wage league, raising critical questions about long-term competitiveness and talent retention in the region.

The Slip from the Podium

According to a comprehensive analysis by insurance provider Trygga, utilizing Eurostat data, Sweden has fallen from the 5th highest-paid country in the EU in 2017 to 8th place today. While Luxembourg retains the top spot with an average annual salary of nearly €83,000—driven by a specialized finance and IT sector—Sweden’s average now sits at approximately €46,525.

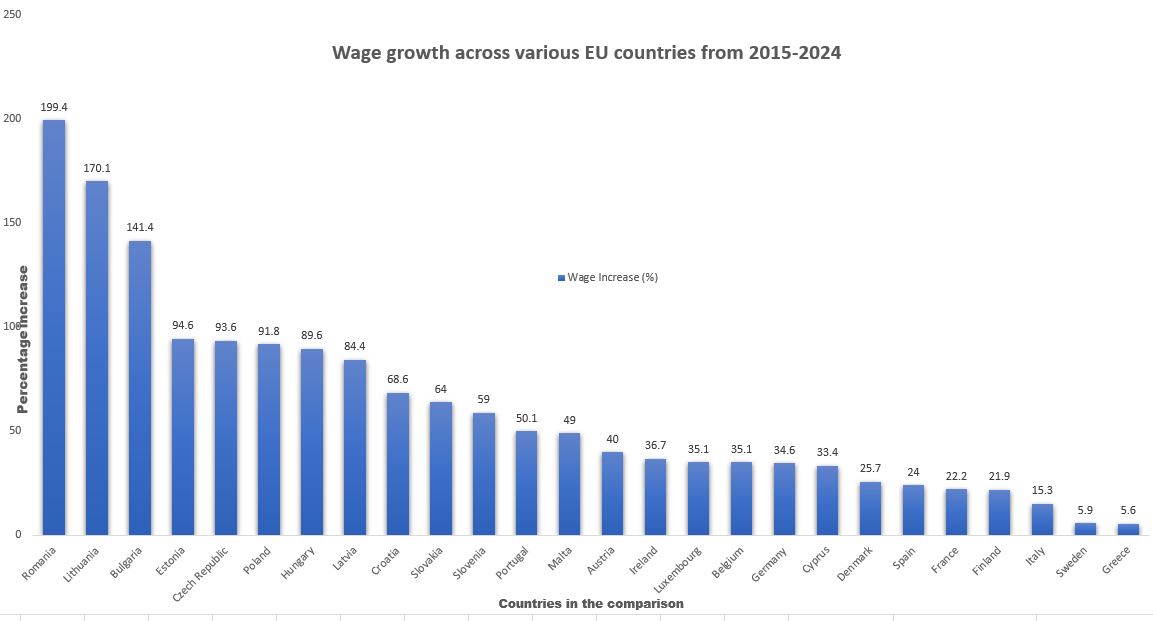

More concerning than the absolute ranking is the trajectory. Since 2015, Swedish wages have increased by only 5.9 percent when calculated in euros. This represents the second-lowest growth rate in the entire EU, surpassed only by Greece, which has been grappling with a decade of economic restructuring. In stark contrast, emerging EU economies are surging. Romania has seen salary growth of 199.4 percent since 2015, with Lithuania and Bulgaria also posting triple-digit increases.

The Currency Illusion vs. Structural Reality

A nuanced analysis requires separating currency fluctuations from real economic performance. Eurostat standardizes data in euros, meaning the Swedish krona’s (SEK) performance heavily influences the ranking. The SEK has weakened significantly against the euro since 2015, driven by divergent monetary policies and lower investor confidence in the Swedish economy compared to its Nordic peers.

Viktor Ström at Trygga notes, “The krona has lost value against the euro during the period—which makes Sweden’s figures look worse than they feel in the wallet.”

However, dismissing this as merely a currency issue would be a strategic error for business leaders. A persistently weak currency often signals underlying economic vulnerabilities, including lower productivity growth and investment hesitancy. Furthermore, even when adjusted for currency, Sweden has lost three ranking positions to neighbours like Finland and economic powerhouses like Germany. This indicates that the issue is not solely exchange rates, but also the pace of nominal wage growth relative to the continent.

The Inflation Shock: Updating the Picture for 2024

To bring this reporting to current times, one must account for the post-pandemic inflation crisis of 2022–2023. While the original data highlights growth since 2015, the last two years have exacerbated the situation. Sweden experienced a spike in inflation that outpaced wage negotiations in the real term for many sectors.

While nominal wages have risen to combat inflation, real wage growth (purchasing power) has been negative or flat for significant periods during this timeframe. When combined with the weak krona, the purchasing power of a Swedish salary for international goods, travel, and investment has diminished. For multinational corporations operating in Stockholm, this creates a paradox: labour costs in SEK may be stable, but the cost of attracting international talent—who compare offers in EUR or USD—has become significantly higher relative to the value provided.

Implications for the Nordic Business Ecosystem

For readers of the Nordic Business Journal, this wage stagnation presents three critical areas of risk and opportunity:

1. The Talent War: As Sweden slips, neighbours like Denmark and Norway (though non-EU, often compared in the region) remain more attractive for high-net-worth professionals. If Swedish salaries do not keep pace with the cost of living and regional competitors, the “brain drain” could accelerate, particularly in tech and engineering sectors where remote work allows employees to earn German or Dutch salaries while living in the Nordics.

2. The Eastern Convergence: The massive wage growth in Romania and Lithuania is not just statistical; it reflects a maturing market. For Swedish companies, this offers opportunities for nearshoring, but it also means these countries are becoming competitors for high-value jobs, not just low-cost manufacturing.

3. The Tax Wedge: Sweden maintains a high tax wedge (the difference between what employers pay and what employees receive). As wage growth stalls, the pressure on the Swedish model increases. Businesses may need to advocate for tax reforms that incentivize higher net income without exploding labour costs.

A Call for Productivity

The slide from 5th to 8th is a warning signal. It suggests that the Swedish economy is failing to generate the productivity gains necessary to sustain its historical wage premium. For the Nordic region, the lesson is clear: reliance on past reputation is insufficient. To maintain the high-wage, high-welfare model, the focus must shift toward innovation, productivity enhancement, and currency stability.

Sweden’s position is not yet critical, but the trend line is pointing in the wrong direction. For investors and executives, monitoring wage development is no longer just an HR metric; it is a key indicator of national economic health and future market viability.

Editor’s Note & Next Steps

Follow-Up Direction:

In our next issue, we plan to deep-dive into “The Nordic Tax Wedge: How Fiscal Policy is Shaping Labor Mobility.” We will analyse how taxation differences between Sweden, Norway, Denmark, and Finland are influencing where top talent chooses to reside and work in 2024.

Connect With Us:

Are you experiencing wage pressure or talent retention challenges in the Nordic region? We want to hear from you. Share your insights for our upcoming report or discuss how these trends impact your business strategy.

- Email: editorial@nordicbusinessjournal.com

- LinkedIn: @NordicBusinessJournal

- Website: www.nordicbusinessjournal.com/contact

Stay ahead of the curve. Stay Nordic.