The announcement — and why it matters beyond the headline

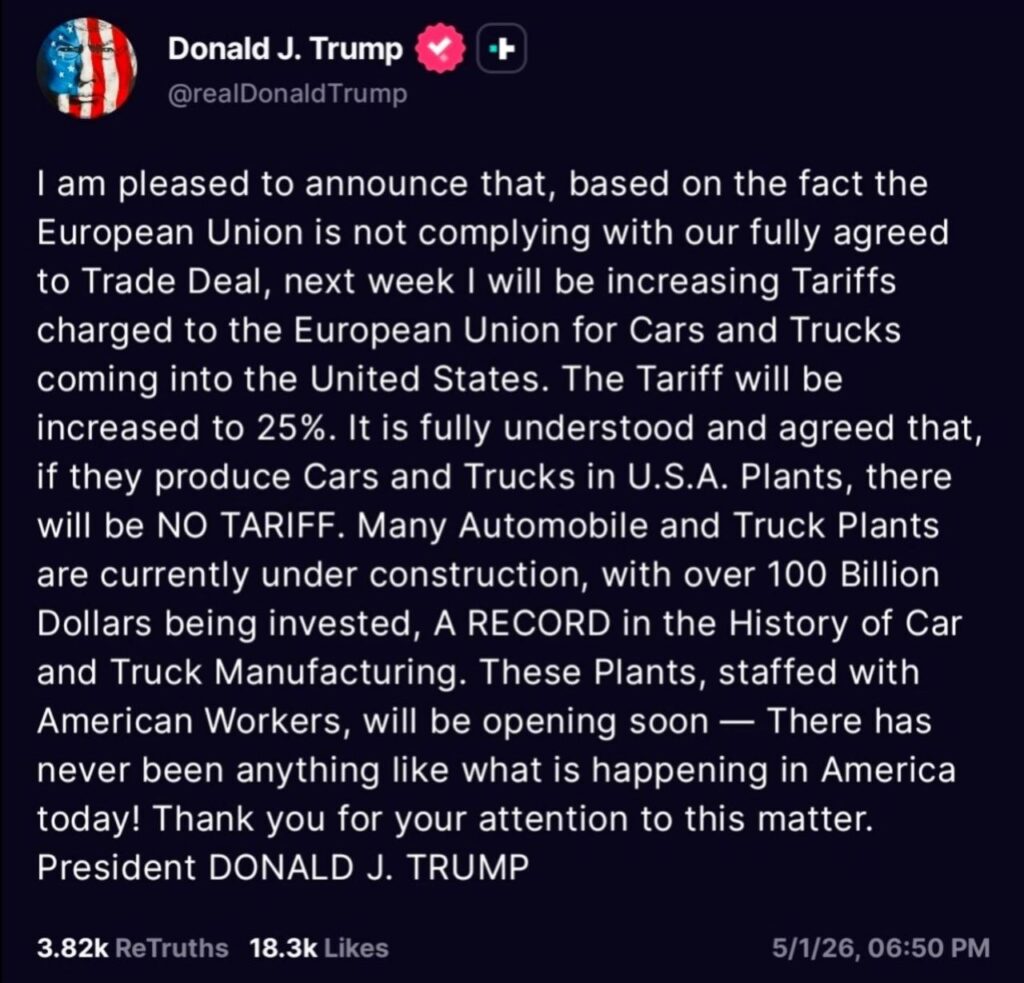

On his platform Truth Social, the U.S. President Donald Trump claimed that import tariffs on European passenger cars and trucks will rise from ~15 % to 25 % “next week.”

No executive order, no congressional bill, no formal notice to the WTO — only a public threat.

For a Nordic business audience, the immediate question is not whether the tariff will take effect tomorrow, but what it signals for supply chains, export margins, and the competitive position of Nordic automakers (Volvo, SAAB legacy suppliers, Tesla Nordic operations, and the dense web of EV component firms in Denmark and Finland).

Even if the move never leaves the realm of political posturing, the expectation of a tariff already distorts pricing, investment timing, and currency risk — and that is enough to affect Q1–Q2 2025 earnings.

The legal reality: why a president cannot simply “raise” tariffs by decree

The constitutional split of power

In the U.S. system, final tariff rates are set by Congress under the Smoot-Hawley Act framework and refined through the Trade Act of 1974 (fast‑track authority).

Presidents can:

- propose new rates or changes,

- invoke temporary national‑security or emergency clauses (e.g., Section 232 steel/aluminium) for a limited period,

- impose proportional counter‑measures under WTO dispute settlements,

but they cannot unilaterally raise permanent ad valorem tariffs on consumer goods such as cars without a congressional vote.

What Trump can do — and has done in the past — is:

1. Issue a “proposed” tariff through a trade‑policy memorandum, creating political pressure on Congress.

2. Use Section 232‑derived safeguards (originally applied to steel & aluminium) to justify broader auto restrictions if linked to “critical supply‑chain security.”

3. Threaten retaliatory action that forces the EU to pre‑emptively negotiate before lawmakers vote.

Thus, in our view, the announcement is less a legal act and more a political instrument to reset the U.S.–EU trade agenda ahead of any potential 2024–2026 presidential term.

Should Europe take this seriously? Historical pattern vs. structural shift

| Pattern | Past behaviour | Current context |

| Posturing → no implementation | 2018–2019 “25 % car tariff” threat collapsed after EU‑U.S. trade talks; 2020 “steel / auto” warnings never materialised. | U.S. Congress is now more fragmented; any tariff lift requires a majority coalition (rare without a national‑security framing). |

| Partial implementation | Section 232 (2018) imposed 25 % on steel / 10 % on aluminium, not cars, after legal push‑back. | Auto supply chains are deeply integrated (Foxconn‑style chip plants in Michigan built by European firms, Nordic battery cells for Tesla/Ford in Kentucky). A blanket 25 % car tariff would trigger immediate industrial retaliation that affects U.S. sub‑contractors, not only EU brands. |

| Negotiation leverage | Threats preceded the 2021–2022 EU‑U.S. Trade and Technology Council (TTC) and the IRA offset discussions. | The 2024 U.S. election cycle + EU Green Deal industrialisation (BATTERIE regulation, REPowerEU) create a window where both sides can trade industrial protection for green‑tech cooperation. |

Bottom line:

Treat the threat as a signal, not a schedule. It forces the EU to pre‑emptively harden its position before any congressional vote is required. The risk is not that the tariff appears next week — it is that a partial version (e.g., on specific models or battery‑chemical content) could be enacted under a national‑security pretext by mid‑2025.

Economic impact on a market already under pressure

High energy prices & auto demand

– EU gasoline/diesel prices have remained ~€1.6–1.8 / L since early 2024 (IEA data), pushing average car purchase prices up 8–10 % versus 2023.

– Discretionary purchase delay is already high: European car sales fell –5 % YoY in Q4 2024 (ACEA).

A 25 % tariff on a €45 k vehicle adds €11 k — roughly the entire margin difference between a mid‑range European model and an equivalent U.S. domestic model after IRA subsidies.

Nordic exposure

– Finland & Sweden: ~18 % of domestic car registrations are imported from the EU (mostly German / Swedish brands); local retailers already report a 12 % drop in high‑end segment inquiries.

– Denmark: strong import market for electric models from Norway (Tesla, Polestar). A tariff would make a $37 k Model 3 effectively $46 k in DKK — crossing the psychological barrier where financing demand collapses.

– Supply‑chain shock: many Nordic component firms (e.g., Norbottens Stål, Danish battery‑pack assemblers) supply both EU and U.S. plants. A tariff would force dual pricing and inventory hoarding before the policy clears — raising working‑capital costs by an estimated 3–5 % for mid‑size suppliers.

Competitiveness & choice

– Model mix: European automakers already struggle to compete with IRA‑subsidised U.S. production (up to $7.5 k per battery‑EV). A tariff erodes that gap, but only for models not produced in the U.S.

→ Nordic EV brands (Polestar, Volvo CE electric machines) that do qualify for IRA credits gain an unexpected shield; conventional combustion models lose price competitiveness instantly.

– Consumer choice: a 25 % levy reduces the number of available models by an estimated 30 % in the upper segment (>$50 k), pushing buyers toward domestic U.S. brands or used‑car markets — both of which increase carbon footprint and strain recycling infrastructure.

The underlying logic: why a tariff now?

1. Political narrative before the election – a visible “America First” move that resonates with industrial‑state voters (Michigan, Ohio) without requiring new spending.

2. IRA leverage – the Inflation Reduction Act already favours U.S. production. A car tariff frames the remaining EU models as “unfair” unless they also relocate production.

3. Battery‑chemical protectionism – U.S. lawmakers are pushing for critical‑mineral supply‑chain security. A car tariff can be paired with a ban on “foreign‑origin battery packs” unless they contain a minimum share of North‑American lithium / cobalt. This hits Nordic battery firms (Northvolt, ESS) that rely on European lithium from Chile/Australia.

4. WTO erosion strategy – by acting outside formal WTO channels, the U.S. tests whether the EU will still enforce dispute‑settlement procedures when the cost of a long litigation is higher than a short‑term price bump.

Free trade, quality & the Nordic value proposition

| Dimension | Current risk | Nordic counter‑argument |

| Free trade | Tariffs re‑introduce non‑tariff barriers, fragmenting the trans‑Atlantic auto market. | The Nordic model (high labour standards, R&D intensity, circular‑economy design) lowers long‑term compliance costs for regulators (less emissions compliance, higher repairability). A tariff ignores these externalities. |

| Quality / design | U.S. consumers associate “European car” with premium build — a tariff erodes that perception by making imports appear “expensive and foreign.” | Nordic firms already lead in modular EV platforms (Polestar 3, Volvo SPA‑EV) that can be produced in the U.S. with minimal retooling. The quality advantage is production‑agnostic; a tariff only punishes consumers, not the technology. |

| Choice & innovation | Less variety → higher price for consumers; loss of R&D diversity (e.g., 4‑wheel‑drive dynamics from Sweden, lightweight aluminium from Finland). | The open‑innovation ecosystem (e.g., Nordic‑U.S. joint labs on solid‑state batteries) creates network effects. Isolating the market destroys the data pools that make those innovations scalable. |

In short: the tariff attacks a symptom (price) while ignoring the cause (the IRA’s asymmetric subsidy regime). The EU’s real response must target the subsidies, not the cars themselves.

What should European / Nordic businesses do now?

1. Inventory & pricing lock‑in – secure 2025 model stock before any tariff window opens; negotiate fixed EUR‑USD pricing with U.S. distributors now.

2. IRA compliance acceleration – if you supply batteries, chips or interior components, begin U.S. production‑qualifying documentation (US‑origin rules of thumb) before any tariff is proposed as law.

3. Diversify customer base – shift a share of export revenue from the U.S. to UK, Japan and emerging Asian EV markets (India, SE Asia) where tariff risk is lower.

4. Political engagement – Nordic MEPs (SEDE, EPP) should push for a joint EU “auto‑origin” definition that treats any car with ≥40 % EU‑made content as “European” for tariff purposes — mirroring the IRA’s domestic‑content test but on the EU side.

5. Supply‑chain localisation – consider small‑scale “near‑shoring” in Midwest U.S. hubs (Indiana, Tennessee) where labour cost is low and infrastructure exists; this turns a tariff from a penalty into a local‑content bonus.

Next Steps & How to Stay in the Loop

What to expect in the next issue

Our follow‑up article (expected Nordic Business Journal, May 2025) will analyse:

– The concrete legislative path: which U.S. congressmen are sponsoring the auto‑tariff bill, the likely vote timeline, and how the EU Trade Commission’s 2025 budget can fund counter‑measures.

– Nordic case studies: quantitative impact models for Volvo Cars USA, Northvolt’s Kentucky plant, and Danish EV‑component exporters under a 25 % scenario vs. a 10 % “battery‑content” alternative.

– Policy playbook: a ready‑to‑use checklist for mid‑size Nordic firms to qualify for U.S. domestic‑content exemptions before the 2026 IRA review.

Connect with us

– Email: editorial@nordicbusinessjournal.com – send company case studies or data for future data‑driven features.

– LinkedIn community: Nordic Business Journal – Trade & Supply Chain (private group for CEOs of <500‑employee firms).

– Newsletter: sign up for the Weekly Trade Brief (every Monday) for real‑time updates on U.S.–EU tariff developments, IRA rule changes, and Nordic export statistics.

The trade war may not start with a signature — but the companies that prepare today will determine which market survives tomorrow.

Article prepared for Nordic Business Journal, April 2025.