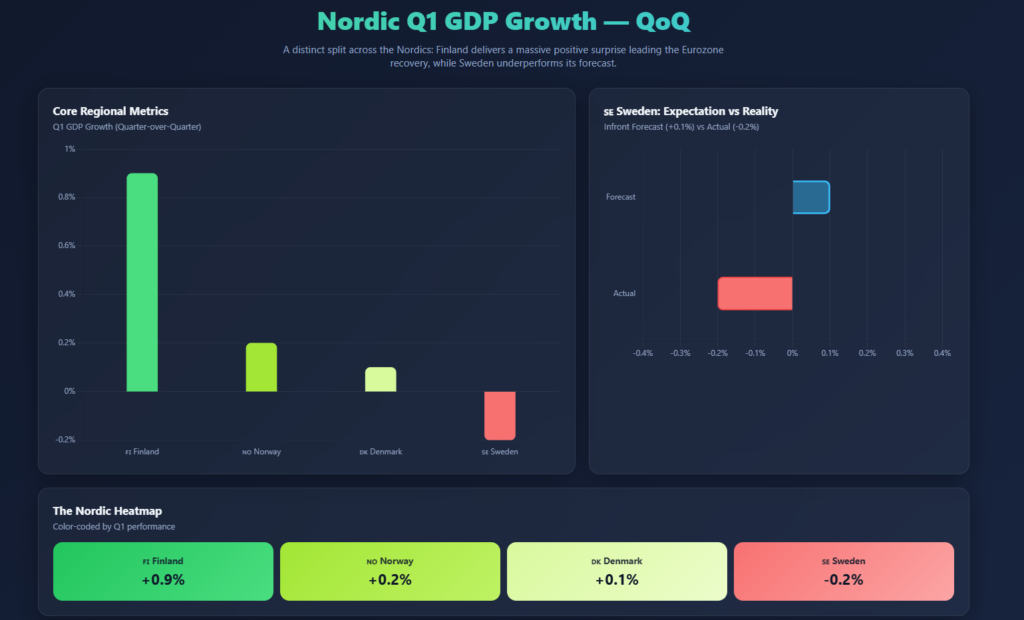

Stockholm — Economists like a predictable trajectory, especially when navigating the delicate tail-end of a global inflationary cycle. For months, the consensus surrounding the Swedish economy was one of quiet optimism. Armed with data tracking stabilising inflation and an expansionary fiscal policy, forecasters at Infront had confidently mapped out a modest, yet reassuring, 0.1 percent expansion for the first quarter of the year. It was supposed to be the quarter where Swedish domestic demand finally shook off its winter coat. Instead, the numbers delivered a cold shower.

According to the flash data released by Statistics Sweden, the nation’s gross domestic product did not climb; it contracted, slipping by 0.2 percent compared to the previous quarter. The discrepancy might seem microscopic on paper—a mere fraction of a percentage point—but in the high-stakes world of macroeconomic forecasting, it represents a jarring disconnect between market assumptions and real-world friction. While analysts expected household consumption to gather pace, a sluggish start in January and February, coupled with a quiet contraction in industrial manufacturing and merchandise exports, effectively dragged the headline figure into the negative.

What turns this minor domestic stumble into a compelling broader narrative, however, is a quick glance across the Baltic Sea and beyond the Scandes mountains. Sweden is not operating in a vacuum, yet it increasingly looks like the region’s structural outlier.

While Stockholm registers an unexpected dip, its Nordic neighbours are painting a vastly different picture of economic resilience. Finland has broken out of its recent quiet period with a resounding 0.9 percent surge, leading the Eurozone’s early-year recovery. Denmark continues to ride the high-octane wave of its powerhouse pharmaceutical exports, and Norway’s economy remains reliably anchored by energy sector strength and robust public spending.

This widening divergence raises an uncomfortable question for policymakers at the Riksbank and the Ministry of Finance: Is Sweden’s Q1 decline merely a temporary, localised blip on an otherwise guaranteed path to recovery, or is the Swedish model uniquely vulnerable to structural headwinds that its closest neighbours have already learned to outmanoeuvre?

Here is the analytical body section for your article. It takes the statistical dip and unpacks it chronologically and structurally, maintaining that engaging, crisp business-magazine tone.

Anatomy of a Stumble: Interest Rates, Weather, and Wholesalers

To understand how Sweden’s economic engine slipped into reverse while its neighbours shifted gears, one has to look beneath the headline GDP figure. The 0.2 percent contraction was not a sudden, dramatic collapse. Rather, it was a death by a thousand cuts—a classic “soft patch” where multiple localized headwinds converged during the first two months of the year.

Chief among these culprits is the lingering hangover of high borrowing costs. While the Riksbank has held its key policy rate steady at 1.75 percent, the lag effect of previous tightening cycles continues to filter through the economy.

Unlike many continental European economies where long-term, fixed-rate mortgages are the norm, Swedish households are uniquely exposed to interest rate volatility. The vast majority of domestic property owners hold variable-rate loans or short-term fixes. Consequently, as those mortgages rolled over, disposable income was quietly cannibalised by debt servicing costs.

“The reality is that Swedish consumers are still fundamentally adapting to a higher-for-longer interest rate reality,” notes a regional macro economist. “Even as inflation cools, the friction inside household budgets remains acute.”

This consumer inertia was compounded by a brutal winter stretch. A prolonged period of unusually cold weather in January and February sent domestic electricity prices spiking. Faced with inflated utility bills and costly mortgages, consumers simply shut their wallets, triggering sluggish winter retail numbers.

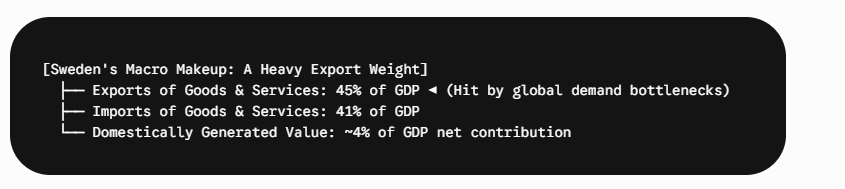

At the same time, the corporate sector faced its own hurdles. A spike in industrial inventories during the first quarter revealed a classic supply-and-demand mismatch: factories kept humming, but the goods began piling up on warehouse shelves rather than moving across the border. Global trade turbulence and temporary manufacturing bottlenecks chilled merchandise export volumes—a heavy blow for an economy where exports of goods and services traditionally command roughly 45 percent of total GDP.

The March Mirage?

Yet, tracking an economy quarter-by-quarter can be deceptive, and Sweden’s Q1 numbers hide a dramatic late-season plot twist. The contraction was heavily front-loaded into January and February. By the time the snow melted in March, a sharp turnaround was already underway.

Driven by a broad-based, 3.1 percent surge in monthly retail sales—partially juiced by an early Easter holiday shopping bump—the monthly GDP indicator for March snapped back by a robust 1.9 percent. Industrial production showed late signs of life, and business confidence held firm.

This dramatic late-quarter swing suggests that Sweden’s economic dip might look more like a temporary winter freeze than a deep structural rot. But while a spring thaw is undoubtedly underway, the slower-than-expected start to the year proves that Stockholm’s path back to sustained growth is bound to be a bumpy ride.

Here is the concluding section to wrap up your feature article, detailing the intricate policy dance between central bank caution and aggressive government fiscal stimulus.

The Policy Tug-of-War: Riksbank Caution Meets Fiscal Stimulus

The unexpected Q1 contraction has left Sweden’s economic stewards navigating a delicate paradox: inflation is hovering safely below target, yet the real economy is shivering. Turning this soft patch into a sustainable spring expansion will require a high-wire act of coordination between monetary policy and newly rolled-out fiscal measures.

At the centre of this balancing act is the Riksbank. Having aggressively pruned the policy rate down from its peak of 4.0 percent to 1.75 percent, the central bank’s Executive Board chose to hold steady at its latest policy meeting.

The rationale behind the pause is clear. While domestic growth remains fragile, external volatility—particularly geopolitical friction and elevated commodity costs—poses a persistent threat of inflationary supply shocks. For the Riksbank, the current strategy is one of watchful waiting, holding the line at 1.75 percent to provide a stable, predictable floor for businesses and homeowners while allowing the previous rate cuts to fully filter into the financial system.

“Inflation outcomes have been lower than forecast, which gives us scope to wait,” noted the Riksbank in its monetary policy assessment. “But the risk of external supply shocks means we cannot declare a total victory just yet.”

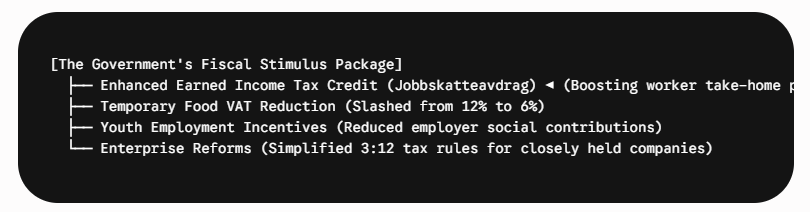

Where central bankers are practicing strategic patience, the Swedish government is stepping in with aggressive relief. The Budget Bill has unleashed a multi-layered wave of tax cuts designed explicitly to inject liquidity back into the private sector, break the economic downturn, and put money back into citizens’ pockets.

The spearhead of this fiscal transition is an enhanced earned income tax credit (jobbskatteavdrag), aimed at boosting take-home pay for workers and individuals over 66. To combat the immediate sting of everyday living costs, the government also deployed a temporary slash to the food VAT—halving it from 12 percent to 6 percent.

For the corporate sector, the relief comes in the form of a temporary reduction in employer social security contributions for workers aged 19 to 23, and a structural overhaul of the notoriously complex “3:12 rules” for closely held businesses. By raising the initial threshold for dividends taxed at the lower 20 percent capital gains rate, policymakers are actively incentivising local entrepreneurs to reinvest and hire.

The Convergence Zone

This dual-track approach—monetary stabilization paired with heavy fiscal priming—is projected to lift Sweden’s real GDP growth back toward 1.8 percent over the course of the year.

However, it introduces a classic macroeconomic tug-of-war. While the government’s tax cuts are essential to revive flatlining consumer confidence and rescue the retail sector from its winter slump, the resulting surge in domestic demand could complicate the Riksbank’s long-term inflation targets.

Ultimately, Sweden’s Q1 contraction was less a sign of fundamental structural decay and more a reflection of an economy transitioning out of an intensive care phase. If the government’s tax reliefs successfully rekindle domestic momentum without sparking a secondary inflation wave, the winter dip will look like a minor speed bump. If not, Sweden may find itself stuck in the slow lane while its Nordic neighbours continue to accelerate away.