Sweden’s Record-Low Birth Rate Signals a Structural Threat to the Nordic Model

In 2024, Sweden recorded a total fertility rate of 1.43 children per woman—the lowest in the nation’s history. This is not merely a demographic footnote. It is an economic alarm bell. For a country that has built its competitiveness on a robust workforce, generous welfare state, and intergenerational social contract, the collapse in family formation represents nothing less than a strategic threat to the Nordic model itself.

The Swedish government has responded with a formal inquiry led by economist Åsa Hansson to investigate why one in four young women now hesitate to have children, compared to one in ten just a decade ago. The findings are expected to reshape family policy, housing regulation, and labour market strategy. But the crisis extends far beyond Sweden’s borders. Across the OECD, fertility rates have fallen to an average of 1.46, well below the 2.1 replacement threshold. The question is no longer whether low fertility matters, but how quickly policymakers can address its root causes before structural damage becomes irreversible.

The Housing-Fertility Nexus: From Social Issue to Economic Imperative

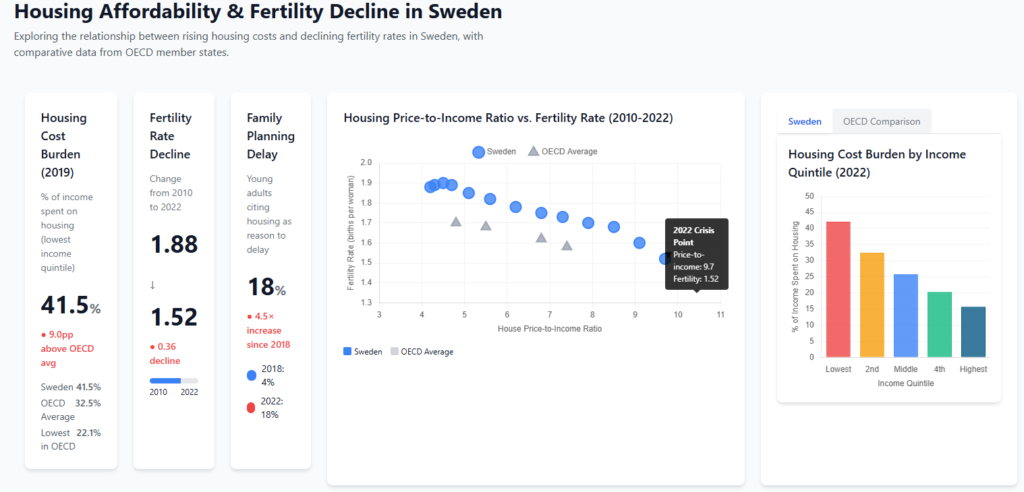

The relationship between housing affordability and fertility decline has moved from academic curiosity to boardroom concern. The OECD’s 2025 Economic Survey of Sweden explicitly links rising housing prices to falling fertility rates across member states, noting that “rising housing prices have also contributed to falling fertility rates across the OECD.” In Sweden, the data is particularly stark: renters in the lowest income quintile spent 41.5% of their income on housing in 2019—significantly above the OECD average of 32.5%.

This is not simply about cost. It is about the “commodification of housing”—the structural shift in which housing is treated primarily as a financial asset rather than a social good. When young adults must choose between mortgage payments and family planning, the economic feedback loop becomes self-reinforcing: housing unaffordability leads to delayed fertility, which shrinks the future workforce, increasing pressure on public finances and economic growth.

The Swedish case illustrates this with precision. The proportion of young adults hesitating to start families due to housing shortages jumped from 4% to 18% in just four years—a 4.5-fold increase that cannot be explained by gradual cultural shifts alone. This aligns with broader OECD research showing that housing affordability discourages childbearing across developed economies, with house price-to-income ratios rising sharply since 2015.

Beyond Housing: The Multifactorial Nature of Demographic Decline

To attribute Sweden’s fertility collapse solely to housing would be analytically incomplete. The decline that began around 2010 was “strikingly similar across different socio-demographic groups,” affecting first-birth rates across all ages and income levels. This universality suggests systemic, society-wide drivers rather than a single policy failure.

Several reinforcing factors demand executive attention:

Economic Precarity and Labour Market Insecurity. Even where housing is accessible, stagnant real wages and the proliferation of gig-economy employment make family planning financially risky. The Nordic labour market, despite strong headline performance, faces structural challenges including labour shortages and the twin green and digital transitions that are reshaping skills demand.

Delayed Partnership Formation. Marriage and cohabitation rates have declined, particularly in the post-pandemic period, compressing the window for biological childbearing.

Work-Life Tensions. Nordic parental leave policies remain globally generous, but the career costs for women—particularly in professional and leadership roles—continue to influence fertility decisions. The paradox is acute: higher female labour force participation correlates with fertility in Nordic countries, yet the quality of that participation matters profoundly.

Educational Attainment. Higher education correlates strongly with lower fertility across all demographic groups, a pattern that intensifies as more young adults pursue extended academic and professional training.

Cultural and Value Shifts. Individualism, environmental concerns, and evolving life priorities have reduced the normative pressure to parent. The OECD’s 2025 Pensions at a Glance report notes that “young men and women increasingly find meaning in life outside of parenthood,” while the normative demands of “good parenting” have grown more intensive.

The critical insight for decision-makers is that these factors are not independent variables—they are interconnected expressions of economic precarity, of which housing is the most visible and burdensome manifestation for young adults.

The Nordic Comparative: Sweden in Regional Context

Sweden is not alone in this demographic challenge, but its position within the Nordic region reveals important comparative dynamics. As of January 2025, the total Nordic population stood at 28.3 million, yet the structural transformation is unmistakable: over the past 25 years, the 0–19 age group has declined by 13%, the working-age population (20–64) by 3%, while the 65+ cohort has surged by 31%.

Iceland and Norway have maintained somewhat more resilient fertility rates and working-age populations, suggesting that policy design and economic structure matter. Finland, by contrast, has seen its working-age population decline by 8% since 1990—the steepest drop in the region. Denmark sits in the middle, with modest population growth but similar fertility pressures.

The Nordic common labour market—celebrating 70 years of free movement in 2024—was designed to foster integration and mobility. Yet demographic convergence across the region means that intra-Nordic labour mobility may soon become a zero-sum competition for scarce working-age talent rather than a collaborative advantage. All Nordic countries except Iceland are projected to fall below the OECD average for working-age population share by 2060.

For investors and corporate strategists, this has immediate implications: labour shortages will intensify, wage pressures will rise in key sectors, and the competition for skilled talent—both within the Nordics and globally—will become increasingly acute.

Global Dimensions: Why This Is Not a Nordic Exception

The temptation to view Nordic fertility decline as a regional anomaly should be resisted. The pattern is global, structural, and accelerating.

East Asia presents the most extreme cases: South Korea’s fertility rate has collapsed to approximately 0.7, Japan sits at 1.2, and China’s demographic trajectory—after decades of policy-induced low fertility—has reached its trough with projections for gradual recovery over the next 40 years. Europe’s “ultra-low fertility club” now includes Germany (1.35), Estonia, and Austria, all below the UN’s 1.4 threshold.

The convergence is striking. In the early 1960s, fertility rates across OECD countries varied dramatically, with standard deviations of 1.31. By 2024, that variation had compressed to 0.29. Developed economies are demographically converging regardless of housing systems, racial composition, or cultural heritage. The common thread is structural: economic precarity, financialised housing markets, and the erosion of the social conditions that once supported family formation.

The highest fertility rates globally remain in the least developed countries—primarily sub-Saharan Africa and parts of South Asia—where development itself is driving the same demographic transition that Europe and North America experienced decades ago. As these regions develop, their fertility rates will follow the same downward trajectory. The global demographic future is not one of regional disparity but of universal convergence at below-replacement levels.

Policy Implications: Housing as Economic Competitiveness

For Swedish and Nordic policymakers, the housing-fertility nexus must be reframed from social policy to economic strategy. The OECD’s 2025 Sweden report identifies the core problem with surgical precision: Sweden’s housing supply per person compares well to OECD peers, but allocative efficiency is poor. Tax subsidies to homeowners inflate land prices, while rent controls create mismatches between housing needs and available units. Construction productivity, though above the OECD average, has flatlined for decades.

The policy prescription is clear: speed up zoning and permitting to increase land supply; limit local technical requirements to facilitate standardisation and automation; improve skills and digitalisation in construction, planning, and process management. These are not merely housing reforms—they are competitiveness reforms.

For the private sector, the implications are equally direct. Companies dependent on Nordic talent pools must anticipate tighter labour markets, rising recruitment costs, and the necessity of more aggressive retention strategies. Industries from healthcare to technology to construction will face workforce constraints that cannot be solved by automation alone. The demographic dividend that powered Nordic prosperity for decades is reversing into a demographic tax.

The Long View: Demographics as Destiny

The most consequential insight for senior executives and investors is that demographic trends operate with long lags and high inertia. Fertility decisions made today shape labour markets 20 years hence. Policy changes implemented now will not show results for a generation. This means that current data—Sweden’s 1.43, the OECD’s 1.46 average—are not snapshots of a temporary condition but leading indicators of a structural reality.

The old-age to working-age ratio will increase sharply across the OECD, placing additional burdens on the working-age population to finance pay-as-you-go pensions and healthcare. The UN’s probabilistic projections for 2064 place the OECD average fertility rate at 1.53 in the median case—but with a 20th percentile of just 1.17 and an 80th percentile near replacement at 1.88. The uncertainty is itself a risk factor for long-term planning.

Past projections have systematically overestimated fertility rates. The 1994 UN edition foresaw an average OECD TFR of 2.01 by 2025; the 2024 edition corrected this to 1.46. Demographers have consistently been too optimistic. Business leaders should not make the same mistake.

Conclusion: The Strategic Stakes

Sweden’s fertility crisis is not a social welfare issue to be managed by family ministries. It is an economic competitiveness challenge that demands attention from finance ministries, central banks, corporate boards, and institutional investors. The housing-fertility nexus is the most visible expression of a deeper structural problem: the erosion of the economic conditions that allow young adults to form families and build futures.

The Nordic model has long been premised on a social contract in which high taxes fund generous welfare, strong labour protections ensure stability, and public investment in housing, education, and childcare enables broad-based prosperity. When that contract breaks down—when housing becomes unaffordable, when wages stagnate, when family formation feels economically irrational—the model itself is at risk.

For decision-makers, the imperative is clear: treat housing policy as economic policy, fertility as a labour market variable, and demographic decline as a strategic risk to be managed with the same urgency as currency fluctuations or supply chain disruptions. The alternative is a slow-motion economic crisis measured not in quarterly earnings but in decades of lost potential.

Editorial Outlook

The Nordic Talent Wars: How Demographic Decline Is Reshaping Corporate Strategy and Regional Competition

The next logical extension of this analysis examines how Nordic companies, investors, and policymakers are adapting to structural labour scarcity. A follow-up article should investigate: the competitive dynamics of intra-Nordic talent migration; how leading firms are redesigning compensation, retention, and automation strategies; the role of immigration policy in offsetting demographic decline; and whether the Nordic model can be re-engineered to sustain productivity with a shrinking workforce. With labour shortages already acute across the region and the green and digital transitions accelerating demand for specialised skills, the intersection of demography and corporate strategy will define Nordic competitiveness for the next generation.

For further analysis, strategic insights, and partnership opportunities, readers are invited to connect with Nordic Business Journal. Our editorial team welcomes contributions from senior executives, institutional investors, policymakers, and researchers shaping the future of Nordic and international business.

To discuss this article, propose collaboration, or explore advertising and thought leadership partnerships, please contact the editorial desk at Nordic Business Journal.

© Nordic Business Journal. All rights reserved.

References

1. Organisation for Economic Co-operation and Development (2025) OECD Economic Surveys: Sweden 2025. Paris: OECD Publishing. Available at: https://www.oecd.org (Accessed: 3 June 2026).

2. Organisation for Economic Co-operation and Development (2025) Pensions at a Glance 2025: OECD and G20 Indicators. Paris: OECD Publishing. Available at: https://www.oecd.org (Accessed: 3 June 2026).

3. Nordic Council of Ministers (2025) State of the Nordic Region 2025. Copenhagen: Nordregio. Available at: https://www.norden.org (Accessed: 3 June 2026).

4. United Nations, Department of Economic and Social Affairs, Population Division (2024) World Fertility Report 2024. New York: United Nations. Available at: https://www.un.org (Accessed: 3 June 2026).

5. United Nations, Department of Economic and Social Affairs, Population Division (2024) World Population Prospects 2024. New York: United Nations. Available at: https://population.un.org/wpp/ (Accessed: 3 June 2026).

Note: The article also references a Swedish government inquiry led by economist Åsa Hansson; however, as this was described as an ongoing formal inquiry at the time of writing, a specific published report was not yet available for citation. Readers should consult the Swedish Ministry of Finance for updated publications.