A structural shift in central bank balance sheets is rewriting the rules of global finance. For Nordic decision-makers, this is not a distant macro trend—it is an immediate exposure and a generational strategic challenge.

In the quiet corridors of central banking, a silent revolution has ceased being unnoticed. On June 2, 2026, the European Central Bank confirmed what reserve watchers had long suspected: gold has overtaken US Treasury bonds as the world’s most common reserve asset. At the end of 2025, gold accounted for 27% of global reserve holdings, against 22% for US Treasuries—a first since the mid-1990s.

Yes, part of that is mechanical: gold’s 60% price surge in 2025 did heavy lifting. But to dismiss this as mere accounting would be a dangerous error. The valuation effect is the signal. It reflects a profound reorientation of how monetary authorities think about risk, sovereignty, and—most critically—trust.

For Nordic executives, investors, and policymakers, this is not an arcane debate about reserve composition. It is a clear warning: the dollar-based financial order that has underpinned global trade and investment since Bretton Woods is fragmenting. The implications for currency risk, capital allocation, and regional competitiveness are immediate.

Why Central Banks Are Buying Gold

| Motivation | Percentage |

|---|---|

| Geopolitical tensions | 31% |

| Inflation hedging | 22% |

| Dollar diversification | 19% |

| Safe-haven demand | 18% |

| Other | 10% |

1. The Signal Beneath the Noise

The ECB report is appropriately cautious: correcting for valuation effects (using end-2023 gold prices), the euro’s share (16%) equals gold’s (16%), and US Treasuries still command a markedly higher 26%. But this caution misses the forest for the trees.

The valuation effects themselves are symptoms of deeper forces:

– Geopolitical risk priced into every major asset class.

– Eroding trust in dollar-denominated paper.

– A structural hunt for what reserve managers now openly call “sanction-proof” stores of value.

Consider the activity, not just the stock. Central bank gold purchases eased to ~850 tonnes in 2025—down from the 1,000+ tonnes of 2022–2024, but still far above pre-pandemic norms. Private investment demand for gold reached nearly 2,200 tonnes in 2025, almost double 2024’s figure, with USD 89 billion flowing into gold-backed ETFs. This is not a temporary spike. This is a generational repricing of risk.

2. The Moment Finance Became a Weapon

The freezing of approximately USD 300 billion in Russian central bank assets after the 2022 invasion of Ukraine was a watershed. It demonstrated a brute fact: dollar reserves held in Western jurisdictions are vulnerable to geopolitical sanctions. For nations with uncertain relationships with Washington—and increasingly for some allies, too—this was an object lesson in the limits of financial sovereignty.

The data are stark. According to OMFIF’s 2025 Global Public Investor survey:

– 31% of reserve managers now cite geopolitics as the most important factor in their investment decisions—up from just 4% a year earlier.

– 96% flagged tariffs and trade protection as their main concern.

– 70% expressed increased worry about the US political environment.

Yet, critically, over 80% still view the dollar as offering safety and liquidity. This is not abandonment. This is hedging. Central banks are not selling Treasuries en masse. They are reducing marginal exposure and diversifying into assets that cannot be frozen, seized, or devalued by a foreign policy shift in Washington.

The geographic pattern of gold accumulation tells the story. Since Russia’s invasion of Ukraine:

– China: +350 tonnes

– Poland: +320 tonnes (a NATO member, notably)

– Türkiye: +220 tonnes

– India: +130 tonnes

These are not random. They are countries that perceive elevated geopolitical risk and are acting accordingly. Poland’s accumulation is especially telling: a staunch US ally building a financial hedge against the very uncertainties that alliance is meant to mitigate.

Gold Overtakes the Dollar

Central bank reserves shift • ECB June 2026

3. Gold’s Paradox: The 2026 Stress Test

Gold’s 60% surge in 2025 and continued climb into early 2026 created a paradox. The metal was celebrated as the ultimate safe haven—until it wasn’t.

During the Iran conflict that began with US-Israeli strikes on February 28, 2026, gold initially spiked from ~USD 5,100 to USD 5,423 per ounce. But when Iran closed the Strait of Hormuz, removing ~20 million barrels per day (20% of global supply), gold plunged. By March, it had hit its lowest level of 2026, underperforming both equities and Treasuries.

The logic is counterintuitive but clear: the oil spike raised inflation expectations, which raised expectations of tighter monetary policy. When real interest rates rise, the opportunity cost of holding non-yielding gold increases. Traders liquidated.

This is the crucial nuance that separates sophisticated from superficial analysis. Gold hedges against geopolitical uncertainty and dollar-specific stress—but not necessarily against inflation-driven rate hikes. For central banks and institutional investors, that distinction is everything. Gold’s diversification benefits shine brightest during financial fragmentation or currency crisis, not during broad-based inflationary shocks.

Morgan Stanley projects USD 5,200/oz in late 2026; J.P. Morgan sees USD 5,000 by Q4, with USD 6,000 possible long-term. But a prolonged Middle East conflict sustaining high oil prices could delay Fed cuts or even prompt hikes, pressuring gold toward USD 4,500. Gold’s trajectory will depend less on geopolitical risk per se than on the interaction between that risk and monetary policy response.From the analysis, these are the most visualization-ready data points:

| Data Point | Value | Source |

|---|---|---|

| Gold share of global reserves | 27% (2026) vs. 20% (2025) | ECB/FT |

| US Treasuries share | 22% (2026) vs. 25% (2025) | ECB/FT |

| Euro share of reserves | ~20% (stable) | ECB |

| Central bank gold purchases | ~850-860 tonnes (2025) | World Gold Council |

| Gold price increase | 55% (2025) | Market data |

| Reserve managers citing geopolitics | 31% (up from 4%) | OMFIF |

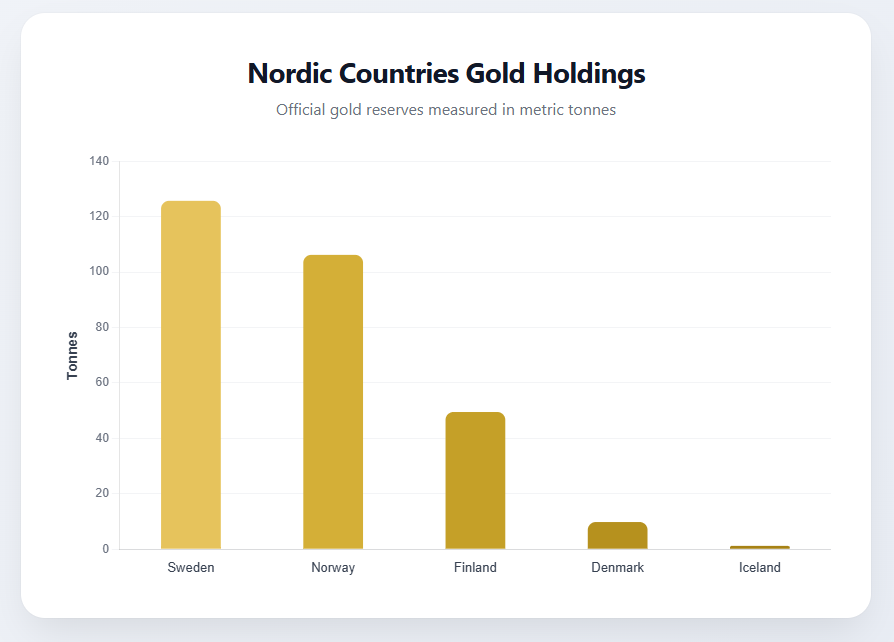

4. Nordic Exposures: The Continuity Bet

The Nordic region is not a passive observer in this shift. It is a case study in contrasting reserve philosophies—and uncomfortable exposures.

Sweden: Confidence or Complacency?

Sweden’s Riksbank holds 125.7 tonnes of gold (market value SEK 161.2 billion as of Dec 31, 2025). Its 2026 strategic allocation left holdings unchanged, with a 70% USD weighting for currency reserves (EUR at 17.5%), gold held separately as a strategic asset.

The Riksbank increased its USD share from 62% to 70% in 2025—even as global trends pointed toward diversification. This is a deliberate bet on dollar continuity.

Yet that bet carries real vulnerability. If de-dollarisation accelerates, or if dollar assets face volatility from US political uncertainty (a concern flagged by 70% of central banks globally), Sweden’s reserve composition could prove suboptimal. The decision not to accumulate gold in 2025, while Poland and others bought aggressively, represents a bet that may or may not pay off depending on how rapidly the financial architecture fragments.

Norway: The Gold-Free Anomaly

Norway presents a striking contrast. Norges Bank sold most of its gold reserves in early 2004; the remainder is explicitly “not considered as part of official reserves.” As of April 2026, official reserve assets stood at ~USD 83.8 billion—with zero gold.

This makes Norway uniquely exposed to the dynamics driving global gold demand. The world’s largest sovereign wealth fund (>USD 1.5 trillion) holds significant dollar-denominated assets. If de-dollarization accelerates, Norway could face indirect pressure on its sovereign wealth, even if central bank reserves are technically separate.

To be fair, the Government Pension Fund Global operates under a different mandate—long-term returns, not liquidity or sanction-resistance. And Norway’s oil-funded fiscal buffer provides insulation most countries lack. Still, the absence of gold is a notable outlier. As central banks worldwide reassess gold as a hedge against fragmentation, Norway’s gold-free stance invites a hard question: is the country adequately diversified against tail risks that are becoming increasingly plausible?

The Regional Pattern: Western Alignment as Risk

The Nordic region generally maintains a Western-aligned reserve posture: heavy USD and EUR allocations. None have been major gold accumulators recently, unlike Poland or Türkiye. This suggests continued trust in the traditional dollar-based system—a stance global trends are increasingly calling into question.

That alignment is not irrational. Nordic economies are deeply integrated into Western financial markets. Their currencies (except the krone) are closely tied to the euro. Liquidity and operational considerations matter.

But the question is whether this alignment remains optimal in a fragmenting world. A net 16% of central banks plan to raise euro holdings—more than for any other currency. For Nordic countries closely tied to European trade, a stronger euro could provide a natural hedge against dollar volatility. Yet the euro’s international role remains constrained by the absence of a full capital markets union and a unified fiscal backstop.

5. The Euro’s Ambivalent Rise

The ECB report notes that the euro’s international role “grew moderately in 2025,” with its composite index up 0.9 percentage points. The euro remains the second most important currency, with a stable ~20% share of official reserves.

International debt issuance in euros reached record highs (>USD 1.1 trillion), and the euro became the leading currency in green and sustainable international bonds (~USD 100 billion). These are real achievements.

But in global FX trading, the euro’s share fell by ~2 percentage points in the BIS triennial survey. More concerning: the Chinese renminbi’s share in global trade finance (Swift) increased from 5.5% in 2024 to ~8% in March 2026, while the dollar’s share fell by >2 points to ~81%. The renminbi now settles nearly a third of Chinese external trade and has surpassed the euro in trade finance—a category where Europe should have natural advantages.

ECB Executive Board member Piero Cipollone warned: “The international monetary system is becoming more contested. Europe cannot afford to be the one that does not act.” For Nordic countries, the euro’s trajectory matters deeply. A stronger international role for the euro could reduce transaction costs and enhance monetary sovereignty. But that requires European-level action on capital markets union—progress that remains painfully slow.

6. Strategic Imperatives for Nordic Decision-Makers

The narrative of gold as an unassailable safe haven requires caveats. Gold is volatile, non-yielding, and costly to store. Its supply is not elastic to liquidity shortages. Central banks need reserves that can be deployed quickly—and gold is poorly suited to that role. That is why >80% of central banks still view the dollar as offering safety and liquidity.

The shift is not away from fiat currencies toward gold. It is away from dollar dominance toward a more diversified portfolio of fiat currencies, with gold as a complementary hedge.

For Nordic institutional investors and corporate treasurers, this nuance is critical. Gold may have a role in diversified portfolios as a hedge against specific risks—financial fragmentation, currency crisis, geopolitical shock—but it is not a panacea. The 2026 Iran conflict demonstrated that gold can underperform precisely when investors expect it to shine, if the shock triggers monetary tightening.

The HSBC Reserve Management Trends 2026 survey found that inflation and interest rates are expected to be the most consequential factors over the next five years. The defining dynamic will be the interplay between geopolitical risk and monetary policy response.

Three Takeaways for Nordic Leaders

1. Concentration risk is rising. Whether in dollars, Treasuries, or any single asset class, the era of unquestioned dollar primacy is ending. Diversification is no longer a theoretical optimisation—it is a risk management imperative.

2. The euro is not a full solution yet. Nordic economies would benefit from a stronger international euro, but Europe must first deliver capital markets union and a genuine safe asset. Until then, the euro remains a regional currency with global ambitions.

3. Review your own “reserve” logic. For corporate treasurers, this means reassessing currency exposure. For institutional investors, it means stress-testing portfolios against a fragmentation scenario. For policymakers, it means asking whether your central bank’s gold posture (Sweden’s heavy dollar bet, Norway’s gold-free outlier status) remains fit for purpose.

Editorial Outlook: The Next Frontier

This analysis has focused on gold and the fragmentation of the dollar-based system. But a critical dimension remains underexplored: digital currencies and tokenised assets.

China’s digital yuan is already in widespread use. The ECB is advancing plans for a digital euro. Private stablecoins and tokenised assets are beginning to challenge traditional payment and settlement systems. How these digital alternatives interact with gold’s analogue renaissance will shape the next decade of reserve management.

A follow-up analysis will examine:

– The strategic implications of the digital yuan for trade and reserves

– Whether a digital euro can overcome the structural limits of its fiat predecessor

– The emergence of tokenized gold and other real-world assets as reserve instruments

– What this means for Nordic monetary sovereignty and financial competitiveness

For Nordic decision-makers, the question is no longer whether the global financial architecture is fragmenting, but how to position for what comes next. The institutions that recognize this earliest will lead. Those that bet on continuity may find themselves exposed.

Nordic Business Journal invites readers to engage with these critical issues. For further insights, partnerships, and discussion, contact the editorial team at editor@nordicbusinessjournal.com or visit www.nordicbusinessjournal.com .

Sources:

- ECB Annual Report on the International Role of the Euro (June 2, 2026);

- OMFIF Global Public Investor 2025;

- Morgan Stanley Research (May 2026); J.P. Morgan Global Research;

- Sveriges Riksbank reserve data;

- Norges Bank reserve data;

- World Gold Council;

- HSBC Reserve Management Trends 2026;

- Financial Times, Bloomberg, Reuters reporting on Iran conflict and gold price dynamics.