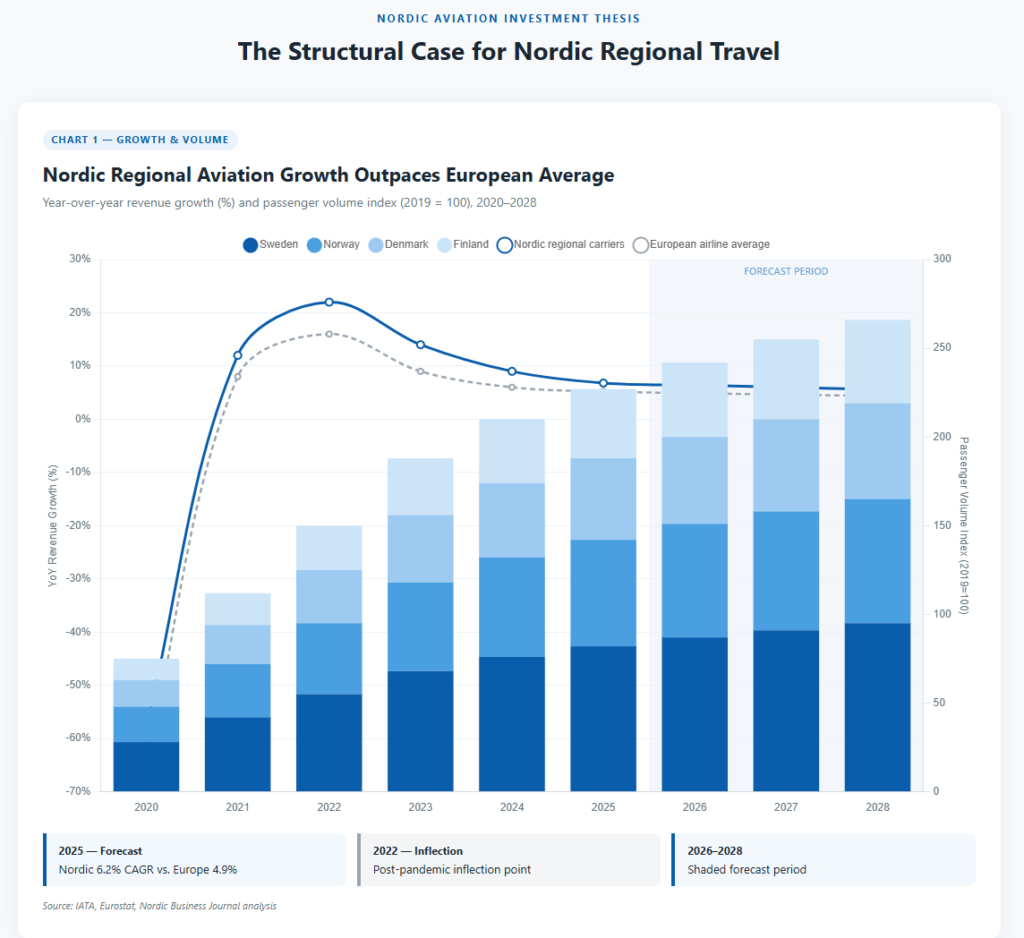

Short-haul and regional air travel in the Nordics is undergoing a structural transformation, driven less by cyclical recovery than by converging macroeconomic, environmental, and regulatory forces. Market projections place regional aviation revenues near $8.93 billion in 2025, with a baseline expansion of approximately 5% year-on-year. Regional carriers are forecasting a 6.2% growth trajectory over the next three years, outpacing the broader European average of 4.9%. Passenger volumes on Scandinavian routes have risen more than 10% annually, while short-haul flight connectivity across Denmark, Finland, Iceland, Norway, and Sweden has expanded by over 12%.

This is not merely a demand surge. It is a market realignment shaped by geographic necessity, shifting climate preferences, geopolitical disruption to global routing, and one of the world’s most aggressive aviation decarbonisation frameworks. For executives, investors, and policymakers, the Nordic short-haul corridor now serves as a live laboratory for how regional connectivity can survive—and potentially thrive—amid fuel volatility, carbon pricing, and technological transition.

Demand Realignment: Geography, Climate Adaptation, and Network Optimisation

The Nordic aviation landscape is inherently distinct from continental Europe’s high-density corridors. Fjords, archipelagos, mountainous terrain, and dispersed population centres limit the economic viability of high-speed rail for many sub-800km routes. Aviation remains the only scalable modal solution for regional cohesion, business mobility, and tourism distribution.

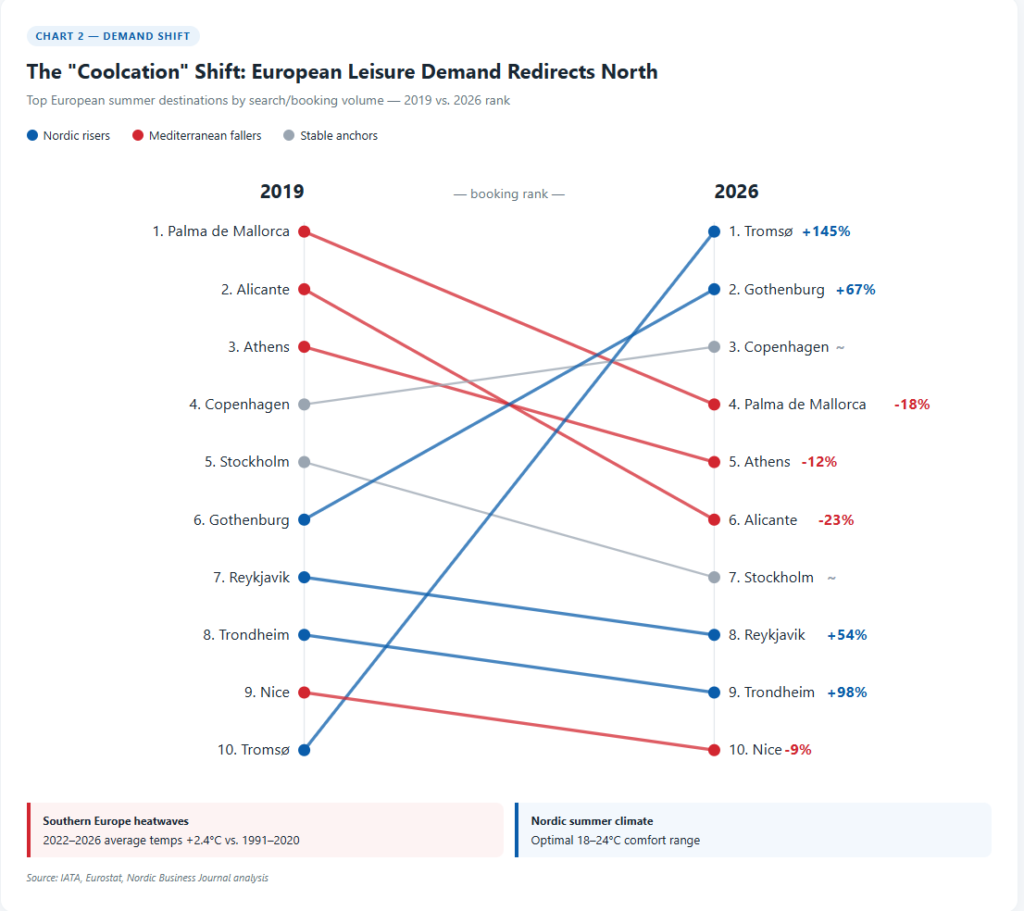

Consumer behaviour has amplified this structural advantage. Persistent heat stress across Southern and Central Europe has accelerated the “coolcation” phenomenon, redirecting leisure demand toward temperate Nordic destinations. Travelers are increasingly booking multi-city regional itineraries to coastal Sweden, Trøndelag, and northern Norway, favouring shorter, cooler hops over traditional Mediterranean fly-and-stay models. Concurrently, high disposable incomes and a cultural emphasis on regional exploration have strengthened domestic short-duration travel.

Airlines have responded through network optimisation rather than brute-force expansion. Legacy and low-cost carriers are recalibrating hub-and-spoke architectures, deepening interline agreements, and deploying right-sized aircraft to maximise load factors on thinner regional routes. The result is higher frequency, improved connectivity, and a more resilient short-haul ecosystem that balances commercial viability with geographic reality.

Geopolitical Friction and the Fuel Economics Reset

The early 2026 escalation in the Middle East, culminating in temporary closures of critical transit corridors including the Strait of Hormuz, triggered a 64% spike in crude prices and a near-doubling of jet fuel costs. The shock reverberated through global aviation economics. Long-haul carriers rerouted around restricted airspace, incurring substantial efficiency penalties. European budget and legacy airlines implemented fuel surcharges ranging from £150 to over £360 per sector, while winter fare adjustments compressed leisure demand on longer routes.

Rather than cancelling travel, European consumers pivoted. The “staycation” and near-holiday trend gained structural traction, with travellers favouring domestic or cross-border regional trips to avoid volatile international pricing and transit hub disruptions. In the Nordics, this localisation of demand reinforced short-haul strength but introduced margin pressure. Operators now navigate a complex cost matrix: elevated fuel and carbon compliance expenses, persistent OEM delivery delays, tight pilot and maintenance labour markets, and the operational burden of severe winter weather.

Capacity discipline has become a strategic imperative. Airlines are prioritising route profitability over network breadth, deploying dynamic hedging strategies, and accelerating fleet modernisation to improve fuel efficiency. For investors, the lesson is clear: short-haul resilience in the Nordics will depend less on passenger growth and more on operational precision, fuel risk management, and fare elasticity control.

The Decarbonisation Mandate: SAF Costs and the Electric Horizon

Fuel volatility intersects with regulatory certainty. The EU’s ReFuelEU Aviation framework, combined with national climate targets, is forcing a rapid transition away from conventional jet fuel. Sustainable Aviation Fuel (SAF) and synthetic e-SAF blend mandates are phasing in aggressively, with compliance costs already visible in fare structures. Industry modelling suggests SAF mandates will add approximately 130 SEK per ticket by 2030, rising to nearly 989 SEK by 2040 as non-fossil blending requirements deepen.

In a region where ticket price sensitivity remains high, these costs threaten to suppress demand unless offset by technological alternatives. The Nordics have positioned themselves as first movers in electric regional aviation, recognising that battery-electric propulsion offers both a decarbonisation pathway and a structural hedge against fuel and carbon pricing.

Norway has legislated a target for 100% zero-emission domestic short-haul flights by 2040, backed by a 1 billion NOK allocation through 2036 for low-emission aviation projects. Denmark has established a 2.85 billion DKK green route fund, active through 2033, to subsidize fully decarbonised domestic corridors and transform regional airports into charging and energy management hubs. These initiatives are increasingly paired with industrial development, notably through Swedish manufacturers such as Heart Aerospace, which are advancing certified electric aircraft optimized for sub-500km regional hops.

The economic logic is compelling: on routes under 400km, electric aircraft could reduce direct operating costs by 30–50% once certification and grid infrastructure mature. Yet near-term bottlenecks remain. Battery energy density, cold-weather performance certification, airport grid upgrades, and state-aid alignment with EU competition frameworks will determine the pace of adoption. Electrification is not a substitute for SAF on longer regional routes; rather, the Nordic market is bifurcating into a dual-technology model where SAF sustains mid-range connectivity and electric propulsion dominates ultra-short hops.

Strategic Positioning: Risks, Capital Allocation, and Policy Alignment

The Nordic short-haul aviation market presents a clear strategic inflection point. For operators, the priority is fleet right-sizing, fuel and carbon cost pass-through mechanisms, and operational resilience against climate and labour constraints. For investors, the opportunity lies in regional airport infrastructure modernization, SAF production and logistics, electric aviation supply chains, and tourism ecosystem diversification. For policymakers, the challenge is ensuring regulatory coherence, coordinating cross-border charging standards, and aligning public subsidies with measurable emissions reductions rather than speculative technology timelines.

Key risks include demand elasticity under sustained fare inflation, fragmentation in national decarbonisation timelines, and the possibility that certification delays could outpace regulatory deadlines. Conversely, the Nordics’ early regulatory clarity, public-private financing models, and geographic suitability for electric short-haul operations create a competitive advantage in the broader European aviation transition.

Long-term, regional connectivity will increasingly be evaluated through a triple lens: economic viability, emissions compliance, and community resilience. Carriers that integrate dynamic pricing, energy-efficient fleet planning, and decarbonization partnerships will capture market share. Those relying on legacy operational models will face margin compression and regulatory friction.

Conclusion

Nordic short-haul aviation is no longer defined solely by passenger growth or seasonal tourism cycles. It is a market shaped by climate-driven demand shifts, geopolitical fuel shocks, and binding decarbonisation mandates. The region’s geography makes aviation indispensable; its regulatory ambition makes transition non-negotiable. Success will require disciplined capital allocation, coordinated policy frameworks, and a pragmatic approach to technological scaling. For executives and investors, the Nordic short-haul corridor is a preview of how regional aviation must adapt globally: smaller, smarter, and increasingly electric.

Editorial Outlook

A strategic follow-up should examine the financing and infrastructure architecture required to scale regional electric aviation. Specifically, an analysis of airport grid capacity constraints, public-private charging infrastructure models, EU state-aid compatibility, and the unit economics of electric versus SAF-powered regional aircraft would provide actionable intelligence for infrastructure investors, aviation policymakers, and fleet planners navigating the 2030–2040 transition window.

Nordic Business Journal | Reader Engagement

For executives, investors, and policymakers tracking aviation decarbonisation, regional mobility, and Nordic market dynamics, Nordic Business Journal delivers independent analysis, strategic briefings, and executive dialogues. Connect with our editorial and research teams for sector insights, partnership opportunities, and tailored market intelligence: editorial@nordicbusinessjournal.com | LinkedIn: @NordicBusinessJournal