Europe’s energy transition enters a more pragmatic phase

As Europe navigates a prolonged period of geopolitical instability, Norway has emerged as one of the continent’s most strategically important energy suppliers. The war in Ukraine, persistent tensions in the Middle East, and concerns over global supply-chain resilience have reshaped European energy policy with remarkable speed. Security of supply — once secondary to decarbonisation targets — is again at the centre of political and industrial decision-making.

Against that backdrop, the Norwegian government has approved a new wave of oil and gas exploration across the Barents Sea, the Norwegian Sea and the North Sea. The decision reflects a broader European reassessment of energy realism: while long-term climate ambitions remain intact, governments and industries are increasingly prioritising reliable, politically stable sources of hydrocarbons during the transition period.

For Norway, the shift represents both an economic opportunity and a strategic balancing act.

Norway strengthens its role as Europe’s energy anchor

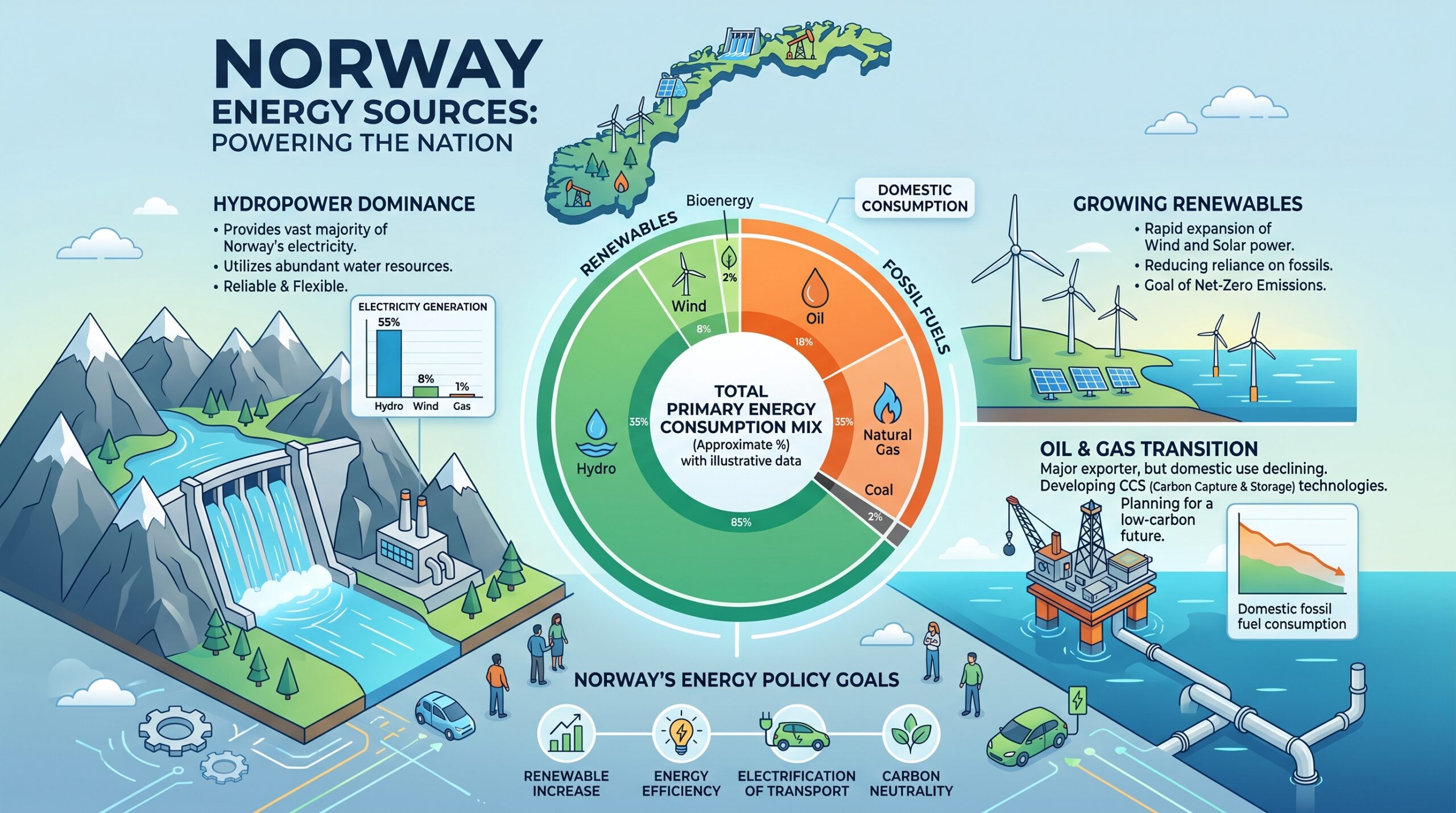

Today, Norway supplies roughly 30% of Europe’s natural gas demand, making it the continent’s largest single gas provider following the sharp reduction of Russian exports after 2022.

Prime Minister Jonas Gahr Støre has framed the country’s expanded exploration programme as a contribution to European stability rather than a retreat from climate commitments.

“Given the war in Ukraine and the situation in the Middle East, Norwegian production is very important,” Støre said in comments to Norwegian media.

The government has authorised exploration in approximately 70 new offshore blocks while also reopening selected mature or previously marginal fields. The strategy aims to extend the productive lifespan of Norway’s continental shelf while leveraging existing offshore infrastructure to reduce development costs and improve commercial viability.

The approach highlights a key distinction increasingly visible in European energy policy: the debate is no longer simply about fossil fuels versus renewables, but about which energy suppliers Europe considers strategically dependable.

In this context, Norwegian hydrocarbons occupy a unique political position. Unlike energy imports tied to geopolitical rivals or unstable regions, Norwegian production benefits from strong institutional credibility, transparent governance, and close alignment with European regulatory standards.

Equinor at the centre of Europe’s energy recalibration

State-controlled energy major Equinor remains central to Norway’s energy strategy. Formerly known as Statoil, the company has evolved into one of Europe’s most influential integrated energy groups, balancing oil and gas production with investments in offshore wind, carbon capture and low-carbon technologies.

Despite volatility in global commodity markets, Equinor has benefited significantly from Europe’s heightened demand for non-Russian energy. As of May 2026, the company’s market capitalisation stands near USD 92 billion, following a strong recovery in energy-sector valuations.

The company continues to pursue aggressive exploration activity on the Norwegian shelf while simultaneously expanding internationally. Reuters recently reported that Equinor plans to substantially increase international oil and gas production by 2030, with major growth projects in Brazil, North America and other offshore regions.

At the same time, Equinor has acknowledged operational limits. CEO Anders Opedal recently stated that the company has little spare production capacity available amid renewed global supply disruptions, underlining how tight international energy markets remain.

For investors, the message is clear: Europe’s energy transition may ultimately reduce hydrocarbon dependence, but the path is proving longer, more complex and more capital-intensive than many policymakers anticipated.

The sovereign wealth advantage

Few countries have converted natural-resource wealth into long-term financial strength as effectively as Norway.

Revenue from offshore oil and gas production continues to flow into the Government Pension Fund Global — commonly known as the Norwegian sovereign wealth fund — now valued at approximately USD 2.1–2.2 trillion, making it the world’s largest sovereign investment fund.

The scale of the fund has transformed Norway into a global financial actor far beyond the size of its domestic economy. Through diversified holdings across thousands of international companies, the fund exerts growing influence over corporate governance, sustainability standards and long-term capital allocation worldwide.

The contrast with many other resource-rich economies remains striking. Norway’s fiscal framework, political consensus and disciplined investment strategy have allowed the country to avoid many of the structural distortions often associated with commodity dependence.

However, the model is not without tension.

As the fund expands, so does scrutiny of how Norway reconciles its climate leadership ambitions with continued fossil-fuel expansion. Environmental organisations and some European policymakers increasingly question whether new exploration activity is compatible with long-term net-zero objectives.

This creates a dual challenge for Oslo: maintaining energy credibility with European allies while preserving its international reputation as a leader in sustainable finance and climate governance.

Europe’s energy transition becomes more pragmatic

Norway’s policy shift also reflects a broader recalibration underway across Europe.

The energy shock triggered by Russia’s invasion of Ukraine exposed structural weaknesses in Europe’s energy architecture — particularly overreliance on imported gas, underinvestment in baseload capacity and insufficient infrastructure resilience.

As a result, many governments are adopting a more pragmatic transition strategy:

- accelerating renewable deployment while maintaining gas as a transition fuel,

- investing in LNG infrastructure and grid modernisation,

- prioritising domestic and allied energy production,

- and reassessing industrial competitiveness in energy-intensive sectors.

For Nordic economies, this evolution carries both risks and opportunities.

Countries with strong renewable capabilities, advanced offshore engineering expertise and stable regulatory environments are increasingly positioned to attract capital. Norway, Denmark and Sweden each stand to benefit from rising demand for energy infrastructure, electrification technologies, offshore services and green industrial development.

Yet the competitive landscape is shifting quickly. The United States’ industrial subsidies, Middle Eastern sovereign investment strategies and China’s dominance in clean-energy manufacturing are intensifying pressure on European policymakers to balance climate goals with industrial policy and economic security.

A strategic window — but not a permanent one

Norway’s energy advantage is significant, but it may also prove time-sensitive.

Oil and gas investment across the Norwegian shelf is projected to decline later this decade as major developments mature and exploration opportunities become more technically challenging. At the same time, Europe’s long-term trajectory toward electrification, hydrogen, carbon capture and renewable energy remains firmly in place.

The central strategic question is therefore not whether hydrocarbons will disappear overnight — they will not — but how producing nations use the remaining window of elevated demand.

Norway appears determined to use that window to strengthen both fiscal resilience and geopolitical relevance. The country is positioning itself not merely as an oil and gas exporter, but as a trusted energy partner during one of Europe’s most complex economic transitions in decades.

For business leaders and investors, the implications extend well beyond energy markets. Norway’s approach offers a case study in how advanced economies can leverage natural resources, institutional trust and long-term capital management to navigate an era defined by geopolitical fragmentation and industrial transformation.

In a world increasingly shaped by strategic dependencies, reliability itself has become a competitive advantage.