Executive summary

After protracted negotiations, EU institutions and member states have moved to implement a tariff agreement with Washington that would see the United States apply a roughly 15 percent duty on a broad set of European goods. The accord—praised by some as a pragmatic way to limit escalation and criticized by others as a poor settlement—forces European businesses and policy makers to choose between immediate predictability and long-term strategic cost. For Nordic exporters, investors and corporate leaders, the deal raises urgent questions about competitiveness, supply‑chain resilience, investment location and transatlantic cooperation at a time when geopolitics and the green transition are already reshaping trade patterns.

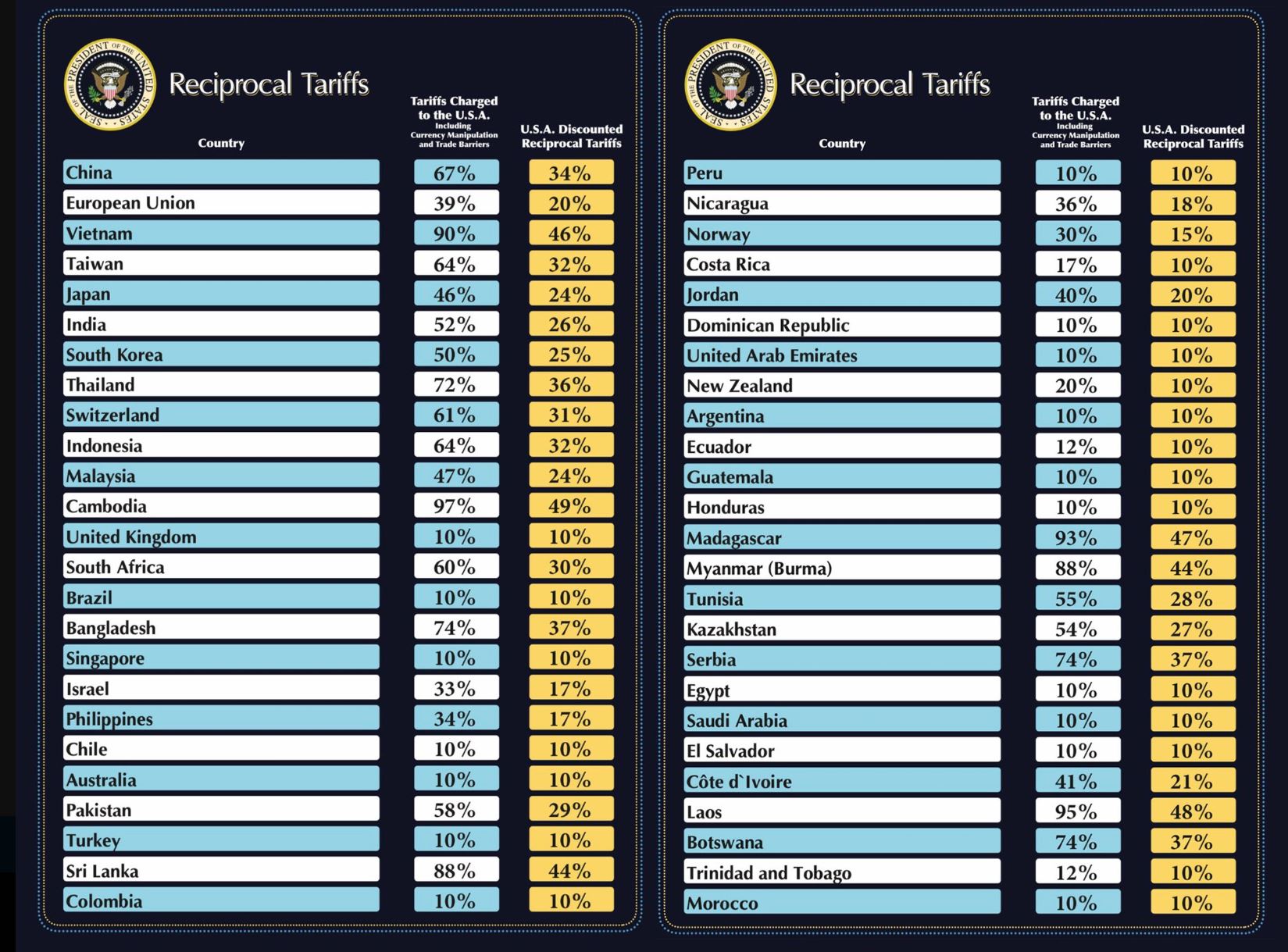

What the agreement means in practice

According to EU negotiators, the practical effect of the deal is an across‑the‑board US tariff of about 15 percent on most European exports. The agreement was reached after intensive talks and has been cleared internally by EU member states and political groups; the European Parliament is expected to vote on final approval in the coming weeks.

Swedish Member of the European Parliament Jörgen Warborn (M), who backs the compromise, described it as “not a particularly good agreement,” but argued the alternative—an uncontrolled escalation into a broader trade war—would be worse. Washington, for its part, set a tight timetable for European approvals; public pressure from the US side forced a faster decision cycle than many in Brussels preferred.

Why this matters now

The deal lands at a precarious time. Global supply chains are still rebalancing after pandemic disruptions and the acceleration of strategic industrial policy: governments are pushing to onshore or nearshore critical manufacturing, decarbonise industry and reassess trade dependence on geopolitical rivals. Introducing sizeable transatlantic tariffs risks raising input costs, shifting investment decisions, and complicating Europe’s green and digital agendas—precisely when industrial investment needs are high.

Nordic exposure and sectoral impact

No Nordic economy is immune, but exposure varies:

Sweden and Finland: High‑value manufactured exports—machinery, automotive components, telecom equipment and specialised industrial goods—face direct margin pressure. Swedish exporters with thin pricing power and long procurement contracts will be vulnerable.

Denmark: Food and pharmaceutical sectors could see selective impacts; Denmark’s life‑science clusters may be partly shielded if exemptions are secured.

Norway (not an EU member): While outside the EU decision, Norway’s exporters would be hit indirectly through integrated European supply chains and potential diversion effects.

Services and digital exports: The immediate tariff structure targets goods, but any trade chill could spill over into services and investment flows that sustain Nordic tech and professional services firms.

Sectors most at risk include autos and components, aerospace, capital goods and certain agricultural and consumer products. Luxury and branded goods may be able to pass on higher costs; commodity‑intensive manufacturers and price‑sensitive exporters will have a harder time.

Economic and market implications

Inflation and margins: A 15 percent tariff on imported inputs and finished goods will tend to raise costs for US purchasers of European goods and for European firms reliant on transatlantic supply chains. The second‑round effects—margin compression, price pass‑through and potential demand destruction—will vary by sector.

Investment and location choices: Firms will reassess investment plans. Expect accelerated rerouting of production toward the US market, increased onshoring or expansion in third markets, and renewed scrutiny of regional production footprints—especially for goods tied to energy transition supply chains (batteries, electrolysers, wind‑turbine components).

Currency and capital flows: Markets will price heightened policy risk into equities tied to export exposure; the euro/dollar exchange rate and country risk premia may react to the news and to the perceived durability of the agreement.

Political calculus and legal options

Brussels’ acceptance appears to be a calculated decision to avoid wider escalation with a strategic partner. But the agreement carries risks:

– Domestic political backlash can be expected from export sectors and opposition parties.

– Legal challenges at the World Trade Organization or through bilateral dispute mechanisms are possible, especially if carve‑outs are unclear or enforcement is uneven.

– The deal may set a precedent for transactional trade diplomacy that complicates longer‑term coordination on industrial policy, climate policy and strategic supply‑chain resilience.

Strategic implications for business leaders and investors

Short-term actions:

– Conduct immediate exposure mapping: quantify revenue and cost exposure by market and product line to understand where the tariff bite is largest.

– Revisit pricing strategies and customer contracts to identify where costs can be absorbed, passed through or hedged.

– Fast-track scenario planning that includes tariff persistence, retaliatory measures and regulatory changes.

Medium‑term responses:

– Reassess supply‑chain topology: diversify suppliers, evaluate nearshoring or regionalisation strategies, and invest in strategic inventory or dual sourcing for critical inputs.

– Accelerate productivity and digitalisation investments (smart manufacturing, automation) to offset higher trade costs.

– Engage proactively with policymakers and trade associations to secure exemptions, transition relief or carve‑outs—particularly for green technologies and critical medical supplies.

For investors:

– Reweight portfolios to reflect sectoral vulnerability and potential winners (companies with strong pricing power, localised production in the US, or unique technology offerings).

– Monitor corporate capital expenditure plans and M&A flows that signal industrial relocation.

Risks to the transatlantic relationship and global trade order

The deal underscores a deeper reality: strategic rivalry, domestic political pressures and industrial policy priorities are increasingly driving trade policy even among allies. If perceived as coercive or unfair, the agreement could erode trust and make future cooperation on climate, technology standards and security harder. Conversely, a pragmatic compromise that limits escalation could provide space for a more constructive negotiation on digital regulation, green industrial subsidies and supply‑chain transparency—if both sides seize that opportunity.

Conclusion — a pragmatic settlement that demands urgent strategic action

Brussels’ choice to accept a difficult tariff compromise reflects a strategic weighing of immediate risks against longer‑term costs. For Nordic and European business leaders, the imperative is clear: move from reaction to strategy. Short‑term hedging and exposure management must be paired with medium‑term investments in resilience, productivity and market positioning. Policy makers should treat this episode as a wake‑up call to deepen transatlantic dialogue on industrial strategy, secure targeted exemptions for climate‑critical industries, and reinforce the rules‑based trade architecture.

This is not just a tariff story. It is a test of how democracies manage economic interdependence while pursuing competitive industrial transformations. Companies and investors who recognise the new strategic landscape and adapt early will preserve optionality and capture the opportunities that inevitably follow market realignment.