Executive Introduction

The Nordic countries—Denmark, Finland, Norway, and Sweden—present a striking economic contradiction. They consistently rank among the world’s most digitally advanced nations, topping global innovation indices and boasting some of the highest living standards on earth. Yet beneath this polished surface lies a troubling reality: a secular decline in labour productivity growth that has persisted since the mid-2000s, corroding the very foundations of the Nordic economic model.

According to the OECD’s 2025 Compendium of Productivity Indicators, labour productivity growth across advanced economies remains anaemic, with the average OECD country seeing growth of just 0.4% in 2024—far below pre-pandemic levels and a fraction of the rates enjoyed in the early 2000s. The Nordics are no exception. While large manufacturing firms have managed to rebound from macroeconomic shocks, the broader economy—encompassing public services, construction, and knowledge-intensive industries—struggles to translate world-class technological infrastructure into measurable output gains.

This paradox matters profoundly for decision-makers. In an era of geopolitical fragmentation, demographic headwinds, and intensifying global competition, the Nordic model’s sustainability depends on resolving the disconnect between digital investment and productivity returns. The question is no longer whether the Nordics can afford to innovate, but whether they can afford not to translate that innovation into economic output.

The Three Fronts of the Productivity Battle

The Nordic productivity slowdown is not uniform. It manifests differently across three critical sectors, each presenting distinct structural barriers and digital frictions that resist simple technological fixes.

Public Services: The Weight of the Welfare Model

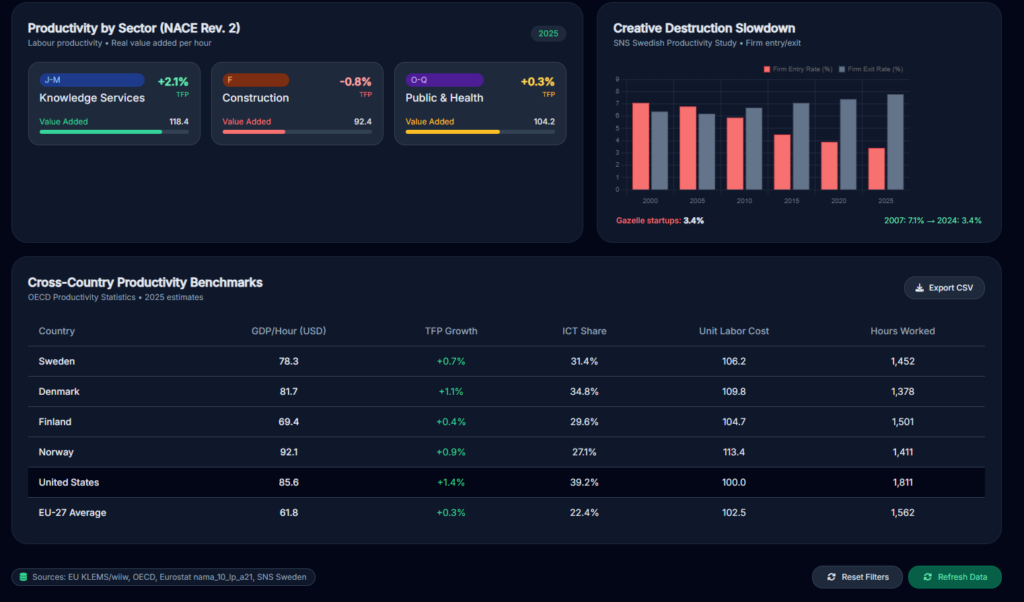

The public sector employs between 31% and 33% of the total Nordic workforce—a proportion that reflects the region’s commitment to comprehensive welfare provision. Yet this very commitment creates a structural productivity ceiling. As economists have long observed, public services such as healthcare, education, and social work are inherently labour-intensive and do not scale easily with technology—a phenomenon known as Baumol’s cost disease.

Nordic governments have invested heavily in citizen portals and digital infrastructure. Denmark’s National Strategy for Digitalisation, Norway’s Digital Norway of the Future strategy, and Sweden’s public sector efficiency initiatives all represent substantial commitments to digital transformation. However, public agencies operate under strict regulatory and data privacy frameworks. To ensure inclusivity for vulnerable populations, they must maintain costly hybrid operating models—running both digital platforms and physical offices simultaneously—which fragments efficiency and bloats operational overhead.

The result is a sector where digitalisation often adds complexity rather than reducing it. Administrative tasks consume an estimated 40% of public sector working time in Denmark alone, according to research by Wilke and the Confederation of Danish Industry. Doctors and nurses in Sweden report that a growing share of their working time is spent on administrative tasks, while the number of patient contacts per doctor has fallen sharply over the past decade—even as the proportion of healthcare administrators has increased significantly.

Construction: Fragmented and Unscaled Operations

Construction projects across the Nordics are highly localised, bespoke, and subject to complex municipal zoning laws and harsh climate realities. While architectural and engineering firms utilise advanced Building Information Modelling (BIM) software, these technological gains fail to spill over effectively to the actual job site. The supply chain remains highly fragmented, relying on a vast network of smaller sub-contractors who lack the capital or scale to adopt integrated digital building systems.

The sector’s productivity challenges are compounded by regulatory bottlenecks. Sweden’s Productivity Commission has identified the functioning of the housing and rental markets as a critical reform area, calling for adjustments to the regulatory framework, increased competition in the construction sector, and stronger incentives for local governments to increase land supply. Without these structural reforms, digital tools remain isolated in design offices rather than transforming the physical construction process.

Knowledge-Intensive Work: The “SaaS Paradox”

Sectors such as professional services, finance, and administrative support have rapidly expanded their shares of the workforce across the Nordics. Yet instead of streamlining operations, an over-abundance of software-as-a-service (SaaS) tools has introduced intense cognitive fragmentation. Knowledge workers spend significant portions of their days managing communication channels, updating redundant databases, and navigating compliance tools.

Research by the Boston Consulting Group reveals a stark reality: Nordic white-collar workers report using generative AI on a weekly basis at a rate of just 19%, compared to a global average of 61%. Nordic users also report saving less than half the time their global peers save through AI use. This “SaaS paradox”—where technology augments peripheral tasks rather than automating core roles—has led to hidden administrative inflation that masks underlying productivity stagnation.

The technology diffusion gap is particularly pronounced between large and small firms. In Sweden, a median manufacturing firm is about 40% as productive as a frontier firm, compared to only 30% in services. The gap in manufacturing has widened since the global financial crisis, indicating that spillovers from highly productive firms to the rest of the economy may be slowing.

Why Advanced Technology Fails to Yield Productivity Gains

Understanding the Nordic productivity paradox requires examining three interconnected structural forces that prevent digital investment from translating into output growth.

The Technology J-Curve and Implementation Lags

Economists have long observed that new, general-purpose digital technologies always suffer from an initial productivity “J-curve.” Buying the technology is fast; inventing the complementary innovations—new organisational workflows, revised management styles, and completely re-engineered business processes—takes years, sometimes decades. The Nordics are currently stuck in this painful transition phase, having invested heavily in digital infrastructure without yet realising the organisational transformations required to extract value from it.

Weakening Creative Destruction

Analysis by the IMF and OECD highlights a slowdown in the “creative destruction” process across the region. In previous decades, highly productive new firms entered the market and pushed out inefficient legacy players. Today, dominant incumbent firms absorb new digital technologies to secure market share, but they do not necessarily optimise their internal labour structures to maximise macroeconomic efficiency. This “sclerosis” of the business landscape prevents the reallocation of resources to more productive uses—a dynamic that is particularly damaging in services sectors where firm-level productivity differences are most pronounced.

The Compressed Wage Structure Challenge

The famous Nordic model relies on a highly compressed wage structure, meaning the salary gap between high-skilled and lower-skilled workers is relatively narrow. While this keeps inequality low and supports social cohesion, it changes the economic calculus for firms: when labour costs are strictly stabilised across service sectors, firms face less raw economic pressure to aggressively replace inefficient human processes with automation. This institutional feature, while socially valuable, may inadvertently dampen the urgency of productivity-enhancing investments.

National Policy Responses: A Comparative Assessment

Each Nordic country has launched ambitious policy initiatives to address the productivity challenge. Their approaches reveal both shared priorities and distinct national strategies.

Sweden: The Productivity Commission’s Comprehensive Reform Agenda

Sweden’s government-appointed Productivity Commission, established in 2023, represents the most systematic attempt to diagnose and address the country’s productivity slowdown. Its interim report, published in 2024, identified a wide set of measures to facilitate resource allocation to more productive firms and sectors. The Commission’s final report, expected in October 2025, will provide detailed recommendations across multiple domains.

Key reform tracks include regulatory simplification, housing market liberalisation, transport infrastructure investment, public sector productivity improvements, and tax system fine-tuning. The Commission has called for simplifying and harmonising regulations to ease the administrative burden on firms—especially smaller ones with limited resources—and improving housing and rental market functioning to facilitate labour mobility.

The IMF’s 2025 Article IV consultation for Sweden endorsed these directions, noting that “improving resource allocation, especially by facilitating labour mobility, and allowing productive firms to scale up rapidly are crucial” for reviving productivity growth. The IMF specifically highlighted the need to protect the creative destruction process, improve innovation market efficiency, and ensure adequate access to finance for SMEs.

Sweden’s 2025 budget also reflects these priorities, with significant allocations for AI and digitalisation (SEK 0.54 billion), improved skills supply, and measures to get more people working. The government has also committed to increasing public investments in research and innovation to at least 1.2% of GDP—a target that TechSverige, the country’s tech industry association, has strongly supported.

Denmark: AI as the Public Sector Transformation Engine

Denmark has taken a distinctive approach, positioning artificial intelligence as the central lever for public sector transformation. In December 2024, the government launched its Strategic Approach to Artificial Intelligence, encompassing three guiding principles—focus on fundamental rights and Danish values, global competitiveness of Danish companies, and ambition to be world-leading in using AI in the public sector—and four national initiatives.

The cornerstone is the Digital Taskforce for Artificial Intelligence, established in collaboration with Local Government Denmark (KL) and Danish Regions. With an earmarked budget of DKK 133.1 million (approximately EUR 17.5 million) for 2024-2027, the Taskforce aims to promote large-scale deployment of AI solutions across the public sector. Its June 2025 report, “More Time for What Truly Matters,” sets ambitious goals: by 2035, AI rollout should free up at least 50 million hours (equivalent to 30,000 full-time positions) across the public sector, with a significant portion achieved by 2030.

The Taskforce’s approach is methodical. It initially prioritises administrative tasks—documentation, resource optimisation, and operations—before expanding to citizen-facing services. Three pilot projects have already received DKK 40.6 million in funding: AI for bone fracture detection, routing and scheduling in healthcare and elderly care, and speech-to-text in healthcare and elderly care.

Denmark’s AI strategy also emphasises building national capabilities. A new Centre for Artificial Intelligence in Society will provide guidance on responsible AI use, while a secure platform for developing transparent Danish language models aims to strengthen the foundation for AI work in both companies and authorities. The initiative to make Danish text data freely accessible as open source represents a recognition that language-specific AI tools are essential for effective public sector deployment.

The IMF’s AI Preparedness Index ranks Denmark second worldwide, indicating strong foundations for harnessing AI benefits. However, the IMF also notes that while 78% of Danes believe AI will benefit companies and 55% believe it will benefit society, only 45% believe it will benefit Danish employees—a trust gap that could slow adoption if not addressed.

Norway: Digitalisation Strategy and AI Infrastructure

Norway’s National Digitalisation Strategy for 2024-2030 sets an ambitious overarching goal: to make Norway the most digitalised country in the world by 2030. The strategy encompasses strengthening governance and coordination in the public sector, ensuring secure digital infrastructure, bolstering cybersecurity, safeguarding privacy, and securing future-oriented digital competence.

On artificial intelligence, Norway has set specific targets: all government agencies should use AI as part of their task management by 2030 (currently 43% do so), and 60% of private sector enterprises should utilise data from the public sector (currently 42%). The government aims to establish a national infrastructure for AI, placing Norway at the vanguard of ethical and safe AI use.

However, an assessment by Implement Consulting Group identifies five key barriers to realising Norway’s AI potential in public administration: fragmented implementation across administrative levels, lack of clear regulatory guidance, procurement practices that risk vendor lock-in, insufficient cross-sector coordination, and a need for more executable and scalable applications. The report recommends establishing a dedicated AI task force to identify, test, and scale cross-cutting AI use cases—suggesting that Norway’s current strategy, while ambitious, may lack the operational machinery to achieve its targets.

Norway’s mainland GDP grew by just 0.6% in 2024, with the IMF projecting 1.5% growth in 2025. The Fund notes that “slowing productivity growth, declining petroleum sector activity, geoeconomic fragmentation, and rising public expenditure pressures—including from defence needs, the energy transition, and an ageing population—pose medium-term challenges to Norway’s generous welfare model.”

Finland: Skills, Innovation, and the Green Transition

Finland’s productivity challenges are perhaps the most acute in the Nordic region. The economy contracted in 2023 and saw minimal growth in 2024, with unemployment rising above 9%. The OECD’s 2025 Economic Survey of Finland identifies skills shortages in firms—including in research—as holding back firm-level innovation, technological diffusion, and productivity growth.

The Finnish Productivity Board has highlighted the need to lift higher education attainment rates that have stagnated since 2000 and to lower barriers to hiring highly skilled foreigners. The EU’s Recovery and Resilience Fund has allocated EUR 1.95 billion (0.7% of GDP) to Finland for projects to boost sustainable growth in digitalisation, green transition, skills, and employment. However, the OECD cautions that “Finland will need to go further to make the most of the green industrial transition,” noting that the growth and productivity return from human capital reforms are modest in the first ten years but more significant after 25 years.

Finland’s enterprise AI adoption has accelerated dramatically, with Statistics Finland reporting that 38% of enterprises deployed AI technologies in spring 2025—up from 24% the previous year. Small and medium-sized enterprises are driving this transformation, with 57% of SMEs now using AI. Yet the gap between organisational adoption and individual usage remains stark: only 16% of individual workers use AI daily, and just 21% have received instruction on using AI in their roles.

The Geopolitical and Competitive Context

The Nordic productivity challenge cannot be understood in isolation from broader global dynamics. The post-pandemic productivity recovery remains fragile and uneven across the OECD, with the 2024 nowcast pointing to an average increase of roughly 0.2 percentage points—far below historical averages. The United States has diverged from other advanced economies, with estimated labour productivity growth of 1.5% in 2024, while most of the G7 experienced negative or near-zero growth.

For the Nordics, this divergence carries strategic implications. US firms are not only investing more aggressively in AI but are also restructuring their organisations to capture its benefits more effectively. The BCG survey revealing Nordic GenAI complacency—lagging global adoption rates by a factor of three—suggests that the region risks falling behind in the next wave of productivity-enhancing technology.

The EU regulatory environment adds complexity. The AI Act, Digital Markets Act, and Digital Services Act create a framework that prioritises ethical deployment and consumer protection—values central to the Nordic model. Yet these regulations also impose compliance burdens that can slow adoption, particularly for smaller firms with limited legal and technical resources. Denmark’s Strategic Approach explicitly addresses this tension, seeking to accelerate AI deployment while maintaining ethical standards, but the balance remains delicate.

Demographic pressures compound the urgency. With ageing populations across all four countries, the working-age share of the population is shrinking, making productivity growth essential for maintaining welfare provision. Denmark’s Taskforce notes that the over-80s currently make up around 5% of the population but are expected to reach 10% after 2047. Without productivity gains, the fiscal sustainability of the Nordic welfare model comes into question.

Strategic Implications for Decision-Makers

The Nordic productivity paradox offers several lessons for senior executives, investors, policymakers, and entrepreneurs:

First, digital investment without organisational transformation is insufficient. The Nordics demonstrate that having the best digital infrastructure does not automatically translate into productivity gains. The critical bottleneck is not technology adoption but technology integration—re-engineering workflows, retraining workforces, and restructuring organisations to capture digital value.

Second, the public sector is both the problem and the potential solution. As the largest employer and service provider in the Nordic economies, the public sector’s productivity performance has outsized macroeconomic implications. Denmark’s AI Taskforce represents a model for systematic public sector transformation, but its success depends on overcoming legal, cultural, and organisational barriers that have resisted previous reform efforts.

Third, the productivity gap between frontier and laggard firms is widening—and this divergence itself drags down aggregate performance. OECD research shows that a 35% increase in the productivity gap between frontier and laggard firms is associated with a 3.5% decline in aggregate multi-factor productivity. For the Nordics, closing this gap requires not just supporting frontier firms but actively facilitating technology diffusion to smaller and medium-sized enterprises.

Fourth, the Nordic model’s social contract may need recalibration. The compressed wage structure, while valuable for social cohesion, may dampen the economic incentives for automation and productivity-enhancing investment. Policymakers face the delicate task of preserving the model’s equity benefits while creating stronger incentives for efficiency gains.

Fifth, AI represents both the greatest opportunity and the greatest risk. If deployed effectively, AI could address the administrative bloat that plagues public services and the cognitive fragmentation that hampers knowledge work. If deployed poorly—or too slowly—it risks adding another layer of technological complexity without resolving underlying structural inefficiencies.

Conclusion: The Decisive Decade

The Nordic productivity paradox is not a temporary aberration but a structural challenge that reflects the deeper tensions of the digital age: between investment and implementation, between innovation and diffusion, between social values and economic incentives. The region’s governments have recognised the stakes and launched ambitious reform programmes. Sweden’s Productivity Commission, Denmark’s AI Taskforce, Norway’s Digitalisation Strategy, and Finland’s innovation investments all represent serious attempts to break the productivity deadlock.

Yet the gap between ambition and implementation remains wide. Technology evolves faster than legislation, organisational cultures resist change, and the complementary investments—in skills, in workflows, in management practices—that turn digital tools into productivity gains require years to mature. The Nordics are in the painful middle of the J-curve, having made the investments but not yet reaping the returns.

The next five years will be decisive. If the Nordic countries can accelerate technology diffusion, streamline public sector operations, and restructure knowledge work to capture AI’s potential, they could emerge from the productivity slowdown with their economic model not merely preserved but strengthened. If they fail, the secular decline in productivity growth will gradually erode the fiscal foundations of the welfare state, forcing harder choices between equity and efficiency.

For international business leaders and investors, the Nordic productivity paradox presents both caution and opportunity. The caution is that digital maturity does not guarantee economic dynamism. The opportunity is that the Nordics possess the institutional capacity, human capital, and technological infrastructure to resolve the paradox—provided they can muster the political will and organisational agility to complete the transformation they have begun.

Editorial Outlook

Follow-Up Angle: “The AI Productivity Dividend: Which Nordic Sectors Will Capture It First?”

A compelling follow-up article would track the implementation of Denmark’s AI Taskforce initiatives, Sweden’s Productivity Commission recommendations, and Norway’s digitalisation targets over the next 12-18 months, assessing which sectors—healthcare, construction, financial services, or public administration—are successfully translating AI deployment into measurable productivity gains. This piece would examine early pilot results, identify best practices in organisational transformation, and assess whether the Nordics are closing the gap with US and Asian AI adopters. It would also explore the emerging role of Nordic AI startups in driving enterprise productivity solutions, and the investment opportunities created by the region’s forced march toward digital efficiency.

Nordic Business Journal invites readers to engage with our editorial team for further insights, partnership opportunities, and discussion on Nordic economic policy and business strategy. Connect with us at editor@nordicbusinessjournal.com or follow our coverage at our various social media sources.

References – Core sources

1. OECD (2025). Compendium of Productivity Indicators 2025. OECD Publishing. — The primary source for cross-country labour productivity growth data, J-curve analysis, and the relationship between frontier-firm productivity gaps and aggregate multi-factor productivity decline.

2. International Monetary Fund (2025). Sweden: 2025 Article IV Consultation—Staff Report. IMF Country Report No. 25/115. — Endorses Sweden’s Productivity Commission reform agenda and provides analysis on resource allocation, creative destruction, and the need for housing market and regulatory reforms to revive productivity growth.

3. Danish Government / Digital Taskforce for Artificial Intelligence (2025). Mere Tid til Det, Der Tæller: Anbefalinger til en Strategisk Indsats for Kunstig Intelligens i den Offentlige Sektor [More Time for What Truly Matters: Recommendations for a Strategic Effort on Artificial Intelligence in the Public Sector]. Copenhagen, June 2025. — The foundational policy document for Denmark’s AI-driven public sector transformation, including the 50 million hour savings target and pilot project framework.

4. Implement Consulting Group (2025). Hvordan Kan Norge Realisere Potensialet for Kunstig Intelligens i Offentlig Forvaltning? [How Can Norway Realise the Potential of Artificial Intelligence in Public Administration?]. — Independent assessment of Norway’s AI strategy identifying five key barriers to implementation and recommending a dedicated AI task force for cross-cutting use cases.

5. Boston Consulting Group (2025). The GenAI Gap: Nordic White-Collar Workers Lag Global Peers in AI Adoption and Time Savings. — Reveals that only 19% of Nordic knowledge workers use generative AI weekly (vs. 61% globally) and documents the “SaaS paradox” of cognitive fragmentation in knowledge-intensive sectors.

This article was prepared for Nordic Business Journal. For reprints, syndication, or speaking inquiries, please contact our partnerships desk.